Last Updated: March 2026 | 12 min read Reviewed for accuracy against current state minimums and average medical cost data. |

| Quick definition: Bodily injury liability (BI) is the part of your auto insurance that pays for injuries you cause to other people in an accident — their medical bills, lost wages, pain and suffering claims, and your legal defense if they sue. It does not cover your own injuries. It does not cover property damage. It covers other people’s bodies when you are at fault. |

I want to start with something most insurance articles skip: the part where everything is fine, and then suddenly it isn’t.

A contractor I know — I’ll call him Dale — ran a red light in Nashville on a Tuesday afternoon back in 2021. Tired, distracted, end of a long week. He T-boned a sedan. Inside: a mother and her teenage daughter. The mother broke her collarbone and cracked two ribs. Her daughter had a concussion and a fractured wrist. Both were hospitalized.

Dale had Tennessee’s state minimum at the time: $25,000 per person, $50,000 per accident. The mother’s hospital bill alone came to $67,000. That didn’t include physical therapy. Didn’t include the eleven weeks she couldn’t work her job as a dental hygienist. Didn’t include what both families’ attorneys were already building in pain and suffering claims before the ink was dry on the discharge papers.

His insurer paid the $50,000 policy limit. Closed the file on a Wednesday. By Friday, both families had lawyers. By the following spring, Dale had a civil judgment hanging over him that his savings account — not his insurer — was going to have to answer for.

That’s the story most people don’t hear when they’re shopping auto insurance. They hear about premiums. They pick the cheapest option. They go home.

This article is about what happens in the gap between the number on your declarations page and the actual cost of a serious accident. I’ve spent seventeen years writing auto policies and watching what unfolds when that gap is too wide.

What Bodily Injury Liability Actually Covers

When you cause an accident and someone else is hurt, your bodily injury liability coverage steps in to pay for:

- Medical treatment

Emergency room visits, surgeries, hospitalization, physical therapy, prescriptions, and follow-up care for anyone you injure.

- Lost wages

If the person you injured can’t work while they recover, your policy can compensate them for that lost income — up to your limit.

- Pain and suffering damages

In serious injury cases, this often exceeds the medical bills themselves. A plaintiff’s attorney will build a pain and suffering argument based on duration, severity, and impact on quality of life.

- Your legal defense

If the injured party sues, your insurer provides a defense attorney. The coverage for this also comes out of your policy limit in most cases.

Here’s what it does not cover: your own injuries. Your own medical bills after an accident you caused aren’t touched by BI — those fall under medical payments coverage (MedPay) or personal injury protection (PIP), which are separate purchases and vary by state.

It also doesn’t cover damage to vehicles or property. The other driver’s car, a fence, a storefront — that’s property damage liability, a completely separate coverage line with its own limit. One accident can trigger both simultaneously.

Bodily injury liability is entirely outward-facing. It exists to compensate people you hurt. Not you.

The Split Limit Structure — and Why the Second Number Is the One That Bites You

Most policies sell bodily injury liability as a split limit: two numbers, written like 25/50 or 100/300. The first number is the maximum payout per injured person. The second number is the maximum payout for the entire accident, regardless of how many people are hurt.

So a 25/50 policy pays no more than $25,000 to any single injured person, and no more than $50,000 total — even if there are six injured people, even if one of them has $180,000 in medical bills.

The moment you hit a minivan with four occupants, that $50,000 gets divided across four injury claims, four sets of legal representation, and four pain and suffering arguments. Fifty thousand dollars divided four ways is $12,500 per person — less than a moderate ER visit in most cities.

Some states and some insurers offer combined single limits (CSL) — one total number that applies across all injured parties with no per-person cap. If your state allows it, it’s worth asking about, especially at higher coverage tiers.

State Minimum Limits: The Numbers, the Context, and the Problem

I’ll say this plainly: state minimum bodily injury liability limits are political artifacts, not actuarial ones. They were set in legislative environments that had no meaningful relationship to what medical care costs, and most states haven’t touched them in decades.

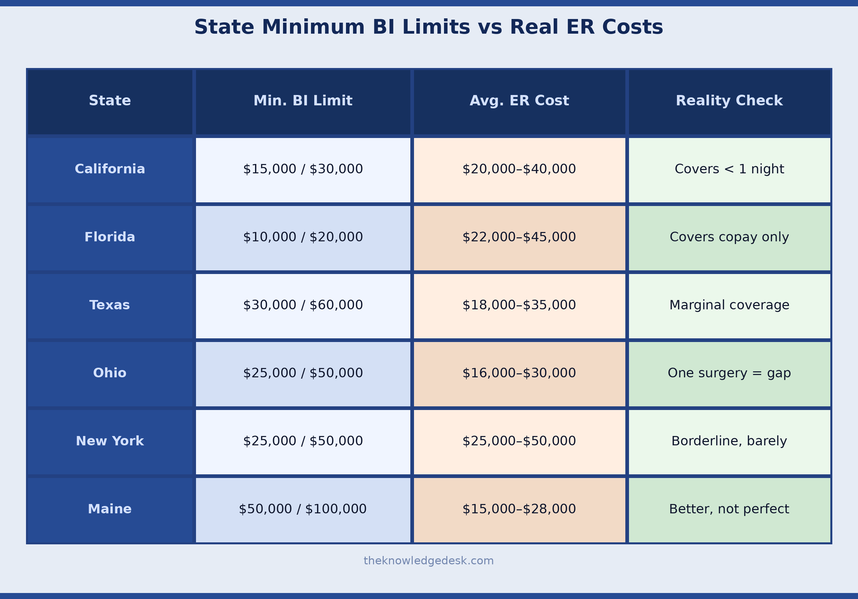

Look at Florida’s minimum — $10,000 per person. A single ambulance ride and three hours in an ER in Miami can exceed that before a doctor has examined anyone. Florida also has some of the highest per-capita litigation rates for auto accidents in the country. That $10,000 isn’t a coverage limit. It’s a down payment.

California sat at $15,000/$30,000 for decades and only recently bumped the minimums — still inadequate for what a single overnight trauma center stay costs. Texas at $30,000/$60,000 sounds better until you price what a herniated disc surgery, six weeks of physical therapy, and eight months of wage replacement looks like for someone in a skilled trade.

Required and adequate are not the same thing in any of these states.

What most experienced independent agents recommend today — and what I tell every client — is a minimum of 100/300 for anyone with assets worth protecting. For clients with a paid-off home, retirement savings, or a stable income that could be garnished, I start the conversation at 250/500 and then talk about umbrella coverage.

What Actually Happens When Your Limit Isn’t Enough

Most articles tell you ‘you could be sued’ and move on. That’s true but incomplete. Here’s what the actual process looks like — because I’ve sat across from clients who’ve lived it.

Step one: your insurer pays your policy limit. They send a release letter to the injured party’s attorney. If the damages exceed your limit — and in serious accidents, they often do — that attorney will almost certainly advise their client to reject the release and pursue the balance through civil litigation.

Step two: a lawsuit is filed. In most states, the statute of limitations for personal injury is two years, sometimes three. Your insurer provides defense counsel, but once your policy limit is exhausted, your legal defense becomes your personal expense.

Step three: a judgment is entered. Once it’s recorded in the court system, the plaintiff’s attorney can file for execution. In most states, that means:

- Wage garnishment — typically up to 25% of your disposable earnings per pay period, continuing until the judgment is satisfied.

- Bank account levies — non-exempt funds in checking or savings accounts can be seized.

- Liens on real property — a lien can be placed on your home, which clouds the title and must be resolved before you can sell or refinance.

And here’s the part most people don’t factor in: judgments accrue interest. In most states, that’s six to ten percent annually, compounding. A $165,000 judgment doesn’t stay at $165,000 while you’re slowly paying it off through garnishment. It grows. By the time it clears, it could be $225,000 or more.

| Real case: A retired schoolteacher in Knoxville — a client I’ll call Margaret — wanted the lowest premium she could get on a fixed income. I wrote her at Tennessee’s state minimum without walking her through the implications as clearly as I should have. Six months later, she rear-ended a pickup truck on a highway on-ramp. The driver had two herniated discs confirmed on MRI, required surgery and eight months of rehabilitation, and was a plumber who couldn’t work for most of that time. Total claim: $190,000. Her policy paid $25,000. A civil judgment for $165,000 was entered against her. Her Social Security income had partial protection under Tennessee law — but her savings account didn’t. She lost most of what thirty years of careful saving had built. I have never written a client at state minimum since that case without explaining exactly what happened to her. I keep that file on my desk. |

Auto Liability Insurance: The Truth Drivers Don’t Know

The Business Use Problem Nobody Talks About Until It’s Too Late

If you use your personal vehicle for any work-related purpose — real estate showings, client visits, deliveries, transporting equipment, or rideshare driving — your personal auto policy’s bodily injury liability coverage may not respond to a claim that happens during that use.

Standard personal auto policies contain business use exclusions. The language typically excludes accidents that occur while the vehicle is being used to carry persons or property for a fee, or while being used in the course of employment. Adjusters with instructions to find that exclusion will find it.

Rideshare drivers are the clearest example. Uber and Lyft provide some coverage during active trips, but the gap period — app on, no passenger accepted yet — has historically had limited coverage from both the personal policy and the platform. That gap has narrowed with some state-level regulatory changes and platform updates, but it hasn’t closed uniformly across the country.

If you use your vehicle for income-generating activity of any kind, the conversation you need to have with your agent isn’t ‘am I covered?’ That question invites a yes. The question is: ‘Show me exactly where in my policy it says I am covered during business use.’

Depending on what you do, the answer might be a business use endorsement, a commercial auto policy, or hired-and-non-owned auto coverage. The cost difference between these options and a claim that falls through the gap is not a close comparison.

Where Umbrella Coverage Fits In

A personal umbrella policy sits above your auto liability limits and picks up once your underlying bodily injury coverage is exhausted. If you carry 100/300 on your auto policy and a judgment comes in at $600,000, your auto policy pays $300,000 and a $1 million umbrella covers the remaining $300,000.

Annual premium for a $1 million umbrella typically runs between $150 and $350 for most households — roughly what you’d spend on a few dinners out. The catch is that umbrella policies require you to carry a minimum underlying limit — usually 100/300 on auto and $300,000 on homeowners — before they’ll attach. That requirement is actually useful: it forces base limits to a reasonable level first.

But I want to be honest about the ceiling here too. Umbrella policies are not unlimited protection. They’re a higher ceiling, not no ceiling.

A client in Atlanta — a careful driver, someone who’d been in the business long enough to know better and had a $2 million umbrella — caused an accident that left another driver permanently disabled. The injured driver was a surgeon. His lifetime lost income claim was calculated at $4.2 million.

My client had 250/500 auto liability plus the umbrella — $2.25 million in total coverage. The judgment came in at $3.1 million. The remaining $850,000 was a personal obligation that meant liquidating investment accounts and a second property he’d owned for twenty years.

I’m not telling you that to make you feel like coverage is pointless. I’m telling you so you understand the real risk spectrum you’re managing. Most accidents don’t produce $3 million judgments. But some do, and the only reason my Atlanta client lost a property instead of everything was because he’d had the umbrella conversation ten years earlier.

How Much Bodily Injury Liability Coverage Do You Actually Need?

The real answer — the one I give clients instead of the industry boilerplate — depends on four things:

- Your net worth. Everything you own above your policy limit is reachable in a civil judgment. Your home equity, your retirement accounts (with some state-specific exceptions), your savings, future wages.

- Your income. Wage garnishment follows you. A judgment entered today can be enforced for years. If you earn a steady income, that income is collectible.

- Your state’s garnishment laws. Some states are more protective of assets than others. Tennessee gives Social Security some cover. Florida has strong homestead protections. Ohio is less forgiving. Your specific exposure depends on where you live.

- Whether you have an umbrella. If you’re carrying 100/300 plus a $1 million umbrella, you have $1.3 million in liability protection. That changes the calculus significantly.

The general framework I use with clients: if you’re a young renter with no significant assets, state minimum is still a risk, but the exposure is lower. If you own a home, have retirement savings, and earn an income that can be garnished — 100/300 is the floor, not the ceiling. Add umbrella coverage. Revisit it when your financial situation changes.

One thing I’ve stopped doing: recommending state minimum to anyone without first having the conversation about what that number means in a real accident. The premium savings on a 25/50 vs. 100/300 policy is often less than $100 a year. The gap in protection is the difference between a closed file and a judgment that follows someone for a decade.

Frequently Asked Questions About Bodily Injury Liability

What does bodily injury liability cover on auto insurance?

Bodily injury liability pays for injuries you cause to other people when you are at fault in an accident. It covers their medical bills, lost wages while they recover, pain and suffering damages, and your legal defense costs if they sue. It does not cover your own injuries, your own vehicle, or any property damage — those require separate coverages.

How much bodily injury liability coverage do I need?

Most licensed agents recommend a minimum of 100/300 — $100,000 per person, $300,000 per accident — for anyone with assets to protect. If you own a home, have retirement savings, or earn an income that could be garnished, that’s the floor. Drivers with significant net worth should consider 250/500 plus a personal umbrella policy. The cost difference between state minimum and 100/300 is often under $100 per year; the coverage difference is enormous.

Does bodily injury liability cover my passengers?

In most states and under most policies, your bodily injury liability does not cover your own passengers — it covers people in other vehicles or pedestrians you injure. Your passengers may need to file under their own health insurance, your medical payments (MedPay) coverage, or an uninsured/underinsured motorist claim depending on the circumstances. This varies by state and by carrier — ask your agent specifically.

What happens if my bodily injury limit isn’t enough to pay all the damages?

Your insurer pays your policy limit and closes its file. If the damages exceed that limit, the injured party’s attorney will typically reject the release and pursue the balance through a civil lawsuit. A judgment can be entered against you personally, followed by wage garnishment, bank levies, and property liens that continue — with interest — until the full judgment is paid. This process typically takes one to three years from accident to active collection.

Is bodily injury liability required in every state?

It’s required in almost every state, but not all. New Hampshire doesn’t require auto insurance at all, though drivers remain personally liable for damages they cause. Virginia until recently allowed payment of an uninsured motorist fee as an alternative. In states that require it, the minimums vary significantly — from Florida’s $10,000 per person to Maine’s $50,000 per person. Being legally compliant and being adequately covered are two different things.

Does bodily injury liability cover accidents during work-related driving?

Not automatically. Standard personal auto policies often exclude accidents that occur during business use — including real estate showings, client visits, deliveries, or rideshare driving. If you use your vehicle for income-generating purposes, ask your agent to show you specifically where your policy addresses business use. You may need a business use endorsement, a commercial auto policy, or hired-and-non-owned auto coverage depending on your situation.

The Conversation Worth Having Before You Need It

Pull out your current insurance declarations page — it’s either in your email, your insurer’s app, or a folder somewhere. Find the two numbers next to Bodily Injury Liability.

If the first number is below $100,000, call your agent this week and ask what raising it to 100/300 costs annually. In most cases, you’ll hear a number that’s smaller than you expect. The gap in protection is not.

And if you own a home, have savings, or earn a salary that matters to your family — that conversation should include umbrella coverage. A thousand dollars a year for $1 million in protection is not a bad trade. Ask me how I know.