Key Takeaways:

- Umbrella insurance kicks in when your regular home or auto insurance hits its limit — protecting your savings, property, and future income

- A $1 million policy typically costs just $150 to $300 per year — one of the best value insurance products available

- It covers lawsuits, serious accidents, defamation claims, and liability situations your standard policies don’t fully handle

- It does NOT cover your own injuries, intentional acts, professional mistakes, or business activities under a personal policy

- Most insurers require minimum liability limits on your underlying policies before they’ll issue umbrella coverage

- Renters, homeowners, landlords, families with teen drivers, and frequent drivers all have good reasons to consider it

Umbrella insurance is a backup layer of liability protection that pays the bills when a lawsuit or serious accident costs more than your regular insurance can cover.

Why This Insurance Exists in the First Place

Here’s the situation umbrella insurance was built for.

You cause a serious car accident. The other driver needs surgery, months of rehab, and can’t work for a year. The total claim lands at $800,000.

Your auto insurance covers $300,000.

Without umbrella insurance, you personally owe the remaining $500,000. That money comes from wherever it can be found — your savings account, your home equity, your investment portfolio, even your future wages through court-ordered garnishment.

With a $1 million umbrella policy, your auto insurer pays its $300,000 first. The umbrella policy covers the remaining $500,000. You walk away financially intact.

That’s the whole point. One bad day — one serious accident, one lawsuit that goes further than expected — can create a financial hole that takes decades to climb out of. Umbrella insurance stops that from happening.

So What Exactly Is Umbrella Insurance ?

Think of your regular insurance policies as the first wall of protection. Your auto policy might cover up to $300,000 in liability. Your homeowners policy might cover $300,000 if someone is injured on your property.

Those limits sound substantial until you price out what a serious injury claim actually costs in the United States — medical bills, lost income, pain and suffering, legal fees. Suddenly $300,000 doesn’t go as far as it seemed.

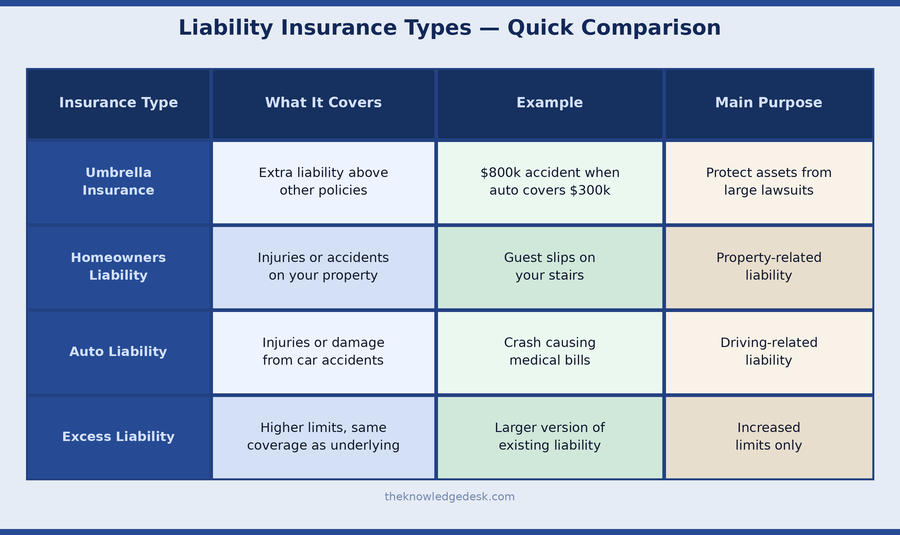

Umbrella insurance is the second wall. It sits above your existing policies and catches everything that falls over the top of them. Most policies start at $1 million in coverage. Many people choose $2 million or more depending on what they have to protect.

The name comes from the way the coverage works — it spreads like an umbrella over multiple areas of risk. Car accidents. Injuries at your home. Certain legal claims. One policy, covering the gaps across several different situations.

Employers Liability Insurance: What it is, why it matters ?

Fiduciary Liability Insurance: Protecting Plan Managers

Real Situations Where It Actually Gets Used

Car accidents are the most common trigger, but umbrella insurance shows up in plenty of other situations that people don’t always anticipate.

A visitor slips on your icy driveway and breaks their hip. Surgery, physical therapy, and lost wages stack up fast. Your homeowners policy covers its limit. The umbrella policy handles the rest.

Your dog bites a neighbour’s child. The injury is serious. The family sues. Medical bills and legal costs push well past what your standard policy covers.

You host a gathering at your home. A guest is injured. You’re found liable. Same story — standard policy pays to its limit, umbrella picks up what’s left.

You post something on social media that someone claims damaged their reputation. They sue you for defamation. Many umbrella policies actually cover personal injury claims like this — something most people don’t realise is included.

An accident happens while you’re travelling internationally. Many umbrella policies provide worldwide liability coverage, not just domestic protection.

Personal vs Commercial Umbrella Insurance

These are two different products for two different purposes, and it’s worth being clear on which one you’re looking at.

Personal umbrella insurance covers individuals and families. It sits on top of your personal auto, homeowners, renters, and boat policies. It’s what most people mean when they talk about umbrella insurance.

Commercial umbrella insurance covers businesses. A construction company facing a multi-million dollar third-party lawsuit after a worksite accident, for example, would use commercial umbrella coverage once its underlying business policies maxed out.

The structure is similar, but the risks, coverage details, and pricing are different. If you’re reading this to figure out whether you personally need umbrella coverage, the personal version is what applies to you.

What Umbrella Insurance Actually Covers

Bodily injury liability — someone gets physically hurt because of something you did or something that happened on your property. Medical bills, lost income, rehab costs, legal settlements. This is the core of what umbrella coverage is built for.

Property damage liability — your actions damage someone else’s property and the claim pushes past your main policy’s limit. The umbrella covers the gap.

Legal defense costs — even a completely false lawsuit costs serious money to defend. Many umbrella policies cover attorney fees and court costs whether you ultimately win or lose.

Personal injury claims — this is the category people most often miss. Libel, slander, defamation, false arrest, invasion of privacy. Someone claims you damaged their reputation or violated their rights. Standard home and auto policies typically don’t touch this. Many umbrella policies do.

Worldwide liability — incidents that happen while you’re travelling abroad can still be covered, depending on your policy.

Rental property liability — some umbrella policies extend to landlords whose liability exposure goes beyond what their landlord insurance covers.

What It Does Not Cover

This matters as much as what it does cover.

Your own injuries and property — umbrella insurance only covers claims made against you by other people. If you’re injured in an accident or your own car gets damaged, that’s what health insurance and your own vehicle coverage handle.

Intentional harm — if you deliberately hurt someone or damage their property, insurance doesn’t cover the consequences. No policy does.

Business activities under a personal policy — if you run a business from home, offer professional services, or have any commercial activity going on, your personal umbrella policy doesn’t cover claims that arise from that. You need commercial coverage.

Professional mistakes — if you give advice in your professional capacity — financial, legal, medical, consulting — and someone suffers losses because of it, that’s professional liability insurance territory. Not umbrella.

Criminal acts, fines, and penalties — nothing in the insurance world covers deliberate criminal behaviour or government penalties.

How Umbrella Insurance Compares to Other Liability Coverage

People mix these up regularly, so here’s the plain version:

The key difference between umbrella and simple excess liability is that umbrella policies sometimes cover risks that your underlying policies don’t cover at all — like those personal injury and defamation claims mentioned above. Excess liability just gives you more of the same coverage you already have.

What Does Umbrella Insurance Cost ?

This is where most people are genuinely surprised.

A $1 million umbrella policy typically costs between $150 and $300 per year in the United States. Adding another million in coverage usually runs an extra $50 to $100 annually.

For most families, $2 million in umbrella coverage costs less than $400 a year. That works out to roughly a dollar a day.

Insurance companies can keep the price this low because umbrella policies almost never get triggered. The vast majority of claims settle within standard policy limits.

But when an umbrella policy does get used, the claims tend to be enormous — which is exactly why having it matters so much.

Your specific premium depends on a few things: how many vehicles you own, whether you have teenage drivers on your policy, whether you own rental properties, and whether your home has features that increase liability exposure — swimming pools, trampolines, large dogs.

Who Should Actually Buy This ?

Umbrella insurance gets marketed as something for wealthy people with a lot to protect. That’s not wrong, but it’s also not the complete picture.

Anyone with significant assets — savings, home equity, investments, retirement accounts. If a lawsuit could reach those, umbrella coverage makes sense. People sometimes forget that future income can also be garnished through court orders. If you’re a high earner, you have something worth protecting even if you don’t feel particularly wealthy.

Homeowners with higher liability exposure — pools, trampolines, and regular gatherings all increase the statistical chance of something going wrong on your property.

Families with teenage drivers — young drivers have statistically higher accident rates. That’s not a judgment, it’s just actuarial reality. Umbrella insurance is often most valuable during the years when teenagers are on the family auto policy.

Landlords — rental properties mean more people on your property, more potential liability, and more ways for a claim to exceed standard landlord insurance limits.

Frequent drivers — the more time you spend on the road, the higher your statistical exposure to a serious accident.

People with public or online presence — if you’re active on social media, run a blog, or have any kind of public platform, the defamation and personal injury coverage in many umbrella policies is worth knowing about.

The Requirement Most People Miss

Here’s something that catches people off guard: umbrella insurance doesn’t work unless your underlying policies maintain certain minimum liability limits.

Most insurers require your auto policy to carry at least $250,000 per person and $500,000 per accident in liability coverage before they’ll issue an umbrella policy on top of it. Homeowners insurance often needs a minimum $300,000 liability limit.

If your underlying policies fall short of those thresholds, there’s a gap — a window where the standard policy has maxed out but the umbrella hasn’t kicked in yet. You’re personally responsible for whatever falls in that gap.

This is why umbrella insurance is usually purchased through the same insurer handling your home or auto coverage. They can make sure everything connects properly with no gaps.

How to Actually Buy It

It’s simpler than most insurance purchases.

Start by checking the liability limits on your current home and auto policies. If they’re below the minimums your umbrella insurer requires, you’ll need to increase them first — which usually costs a little more on those policies but is worth doing.

Figure out what you’re actually trying to protect. Add up your savings, home equity, investments, and think about your future earning potential. That number gives you a sense of how much umbrella coverage makes sense.

Contact the insurer that handles your home or auto coverage first. Bundling umbrella with existing policies almost always gets you a discount and eliminates coverage gap headaches.

Choose a limit that fits your situation. Most people start at $1 million. People with more substantial assets typically go to $2 million or $3 million. The jump from $1 million to $2 million usually costs less than $100 extra per year — which is almost always worth it.

Frequently Asked Questions About Umbrella Insurance

What is umbrella insurance in simple terms? It’s extra liability coverage that pays when a lawsuit or serious accident costs more than your home or auto insurance can cover. It protects your savings and assets from large claims.

Does umbrella insurance cover lawsuits? Yes — lawsuits involving bodily injury, property damage, and certain personal injury claims like defamation are exactly what umbrella insurance is designed to handle.

Can renters get umbrella insurance? Yes. Renters can buy umbrella coverage as long as they also carry renters insurance with the required minimum liability limits.

Does it cover car accidents? Yes. Auto accidents are one of the most common situations where umbrella policies actually get used.

How much umbrella coverage do I need? A common starting point is $1 million. People with significant assets — home equity, savings, investments, high income — often choose $2 million or more. The additional cost per million is small enough that going higher rarely hurts.

Does umbrella insurance cover me abroad? Many policies do include worldwide liability coverage. Check your specific policy terms to confirm.

Is umbrella insurance worth it? For most homeowners, anyone with teenage drivers, landlords, and people with meaningful assets — yes. The cost is low enough and the potential exposure is large enough that it’s hard to argue against it.

What’s the difference between umbrella and excess liability insurance? Excess liability just gives you higher limits on your existing coverage. Umbrella insurance can also cover types of claims that your underlying policies don’t cover at all — like defamation or personal injury claims.

Does umbrella insurance cover my business? Not under a personal policy. Business-related liability requires commercial umbrella coverage.

Can I get umbrella insurance without homeowners insurance? Typically no — most insurers require you to carry underlying home or auto policies with minimum liability limits before issuing an umbrella policy.

The Bottom Line

Umbrella insurance is not something you buy expecting to use it. Most people who carry it never make a claim against it. That’s actually the point.

What you’re buying is the knowledge that one bad day — one serious accident, one lawsuit that takes on a life of its own — won’t dismantle everything you’ve built financially. For somewhere between $150 and $400 a year, that kind of peace of mind is genuinely hard to argue with.

It’s not flashy insurance. It doesn’t cover your phone screen or your travel disruptions or your pet’s vet bills. It covers the scenario where someone sues you for $800,000 and your regular policy only goes to $300,000.

That scenario is rare. But when it happens to people without umbrella coverage, the financial consequences can follow them for the rest of their lives.

Don’t be that person. The coverage is cheap. The alternative is expensive.