Key Takeaways:

- Auto liability insurance pays for other people’s injuries and property damage when you cause an accident — it does not cover your own car or your own injuries

- Almost every state requires it — driving without it risks fines, license suspension, and personal financial ruin

- Policies come with limits — if damages exceed those limits, the difference comes out of your own pocket

- Minimum state-required coverage is almost always dangerously low compared to what accidents actually cost

- Most insurance professionals recommend 100/300/100 coverage as a realistic baseline

- A single serious accident without adequate liability coverage can follow you financially for years

Auto liability insurance pays for the injuries and property damage you cause to other people in a car accident — up to your policy limits — and without enough of it, one bad day on the road can turn into a financial problem that takes years to recover from.

Nobody Thinks About This Until They Need It

You’re driving to the grocery store on a Tuesday afternoon. Nothing unusual. You’ve done this route a hundred times.

Then, in one distracted second, you rear-end the car in front of you at a red light.

Suddenly your mind is moving in five directions at once. Is everyone okay? How bad is the damage? What happens now? And then, quietly underneath all of it — will my insurance actually handle this?

That last question is the one most drivers have never honestly answered. They pay their premium every month, they know they have car insurance, but the specifics of what it covers — and more importantly, what it doesn’t — are a mystery until the moment those details start to matter enormously.

Auto liability insurance is the coverage that pays for the other person’s problems when you cause an accident. Understanding it before something happens is the difference between a stressful afternoon and a financial crisis that drags on for years.

Cyber Liability Insurance: What It Covers & Why It Matters

Why Umbrella Insurance Might Be the Smartest $200 You Spend

What Auto Liability Insurance Actually Is

Here’s the core of it, plainly stated:

Auto liability insurance pays for damage or injuries you cause to other people when you’re at fault in an accident. It does not pay for your own injuries. It does not fix your own car. Its entire job is to protect other people — and by extension, your bank account — from the financial consequences of a mistake you make behind the wheel.

Picture this. You run a red light and hit another car. The driver breaks their arm. Their car is totalled. Your liability insurance covers their medical treatment, their lost wages while they recover, and the cost of their vehicle — up to your policy limits.

Without that coverage, every one of those costs falls on you personally.

Nearly every state in the US requires drivers to carry at least some liability coverage. Drive without it and you risk fines, having your license suspended, and in an accident, being personally responsible for every dollar of damage. The legal requirement exists because the alternative — uninsured drivers causing injuries and property damage they can’t pay for — is worse for everyone.

The Two Types of Coverage Inside a Liability Policy

Auto liability isn’t one thing — it’s two distinct protections packaged together.

| Coverage Type | What It Pays For | Example |

| Bodily Injury Liability (BI) | Medical expenses, lost wages, legal costs, pain and suffering for people injured in an accident you caused | The driver you hit needs surgery and months of physical therapy |

| Property Damage Liability (PD) | Repairs or replacement of property your vehicle damages | You hit another car, a fence, a parked vehicle, or a building |

Both work together. One handles the human cost. The other handles the physical damage. You need both, and they come standard in any liability policy.

Understanding Your Limits — This Is the Part That Actually Matters

Every liability policy has limits — the maximum your insurer will pay after a single accident. These are written as three numbers, like 25/50/20. Most people have seen these numbers on their declarations page and never really thought about what they mean.

Here’s what they actually mean:

| Policy Number | What It Means |

| 25 | Maximum $25,000 paid for one injured person |

| 50 | Maximum $50,000 paid for all injured people combined |

| 20 | Maximum $20,000 paid for all property damage |

So with a 25/50/20 policy, if you cause an accident that injures two people — one with $30,000 in medical bills and another with $35,000 — your insurance pays $25,000 toward each person, $50,000 total. The remaining amounts become your personal problem.

That gap — between what your insurance covers and what the accident actually cost — is where people’s finances get destroyed.

Minimum Coverage vs What You Actually Need

Most states set a legal minimum for liability coverage. And most of those minimums are genuinely inadequate for what accidents cost in the real world today.

| Coverage Level | Bodily Injury Per Person | Bodily Injury Per Accident | Property Damage |

| Typical state minimum | $25,000 | $50,000 | $20,000 |

| Recommended protection | $100,000 | $300,000 | $100,000 |

A single night in a hospital can easily cost $20,000 or more. A serious injury involving surgery, rehabilitation, and lost income can run into six figures without much difficulty.

Modern cars are full of sensors, cameras, and complex electronics — a straightforward-looking rear bumper repair on a newer vehicle can cost $3,000 to $5,000.

The minimum coverage that satisfies the legal requirement in your state was designed to keep you on the right side of the law. It was not designed to actually protect you financially.

Most insurance professionals recommend 100/300/100 as a realistic baseline for anyone with assets worth protecting.

The premium difference between minimum coverage and 100/300/100 is often much smaller than people expect — sometimes $20 to $40 per month — for coverage that is four times more protective.

What Liability Insurance Does NOT Cover

This is where the surprises happen and where people feel let down by their own policy.

Your own injuries — if you cause an accident and injure yourself, liability insurance pays nothing toward your own medical bills. That’s what personal injury protection (PIP) or medical payments coverage is for.

Your own car — if you cause a crash, liability insurance doesn’t repair your vehicle. You need collision coverage for that.

Commercial use — if you’re delivering food, driving for a rideshare app, or using your car for any business purpose, most personal liability policies exclude accidents that happen during those activities. Separate commercial or rideshare coverage is needed.

Intentional acts — if damage was caused deliberately, no insurance company will cover it.

Racing — any accident that happens on a track or during any form of racing is excluded.

None of these exclusions are buried in fine print to trick you. They’re standard across the industry. But not knowing about them until you need to make a claim is genuinely costly.

Employers Liability Insurance: What it is, why it matters ?

Why Landlord Insurance Is a Must for Rental Property Owners?

Liability Insurance vs Full Coverage: What’s the Difference ?

“Full coverage” is a term that gets thrown around constantly and confuses a lot of people. It’s not actually a specific policy type — it’s informal shorthand for a combination of coverages.

| Feature | Liability Only | Full Coverage |

| Covers damage to others | Yes | Yes |

| Covers your own car | No | Yes |

| Covers theft or vandalism | No | Yes |

| Required by law | Yes | Usually not |

| Typical cost | Lower | Higher |

Full coverage typically means liability plus collision (repairs your car after an accident) plus comprehensive (covers theft, weather, fire, and non-collision damage).

If you’re financing or leasing a vehicle, your lender almost certainly requires full coverage — they want the asset protected.

If you own your car outright, the decision about whether to carry full coverage comes down to whether the vehicle’s value justifies the additional premium.

What full coverage does not change is your liability limits. You can have full coverage with dangerously low liability limits. The two decisions are separate.

What Happens When Your Limits Aren’t Enough

This is the scenario that keeps insurance professionals up at night — and should concern every driver.

If you cause an accident and the total damages exceed your liability limits, the injured party can pursue the remaining amount directly from you. That means your savings. Your home equity. Your wages — courts can order garnishment of future income to satisfy a judgment.

A 25/50/20 policy in an accident that causes $200,000 in medical costs leaves $150,000 of exposure sitting with you personally.

This is exactly why umbrella insurance exists. An umbrella policy adds an additional layer of liability protection — typically starting at $1 million — above your auto and home policies.

For most people it costs $150 to $300 per year. For anyone with meaningful assets, it’s one of the most cost-effective insurance decisions available.

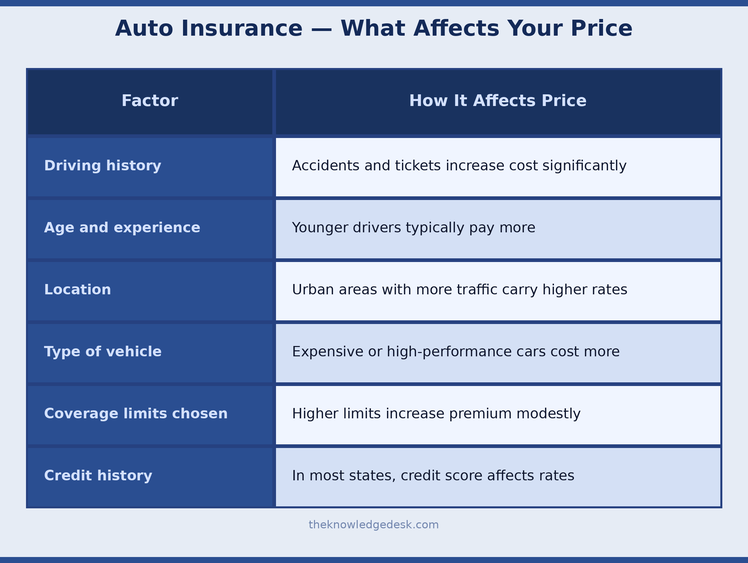

What Determines What You Pay

Premiums vary significantly between drivers. Insurers look at a range of factors when calculating your rate:

Drivers with clean records and several years of experience often pay dramatically less than newer drivers or those with recent violations.

Most insurers also offer discounts for bundling home and auto policies, insuring multiple vehicles, completing defensive driving courses, or having certain safety features in your car.

If you haven’t compared rates recently, it’s worth doing. The market is competitive and your rate from three years ago may not be the best available rate today.

Mistakes Drivers Make With Liability Coverage

A few patterns come up repeatedly when people find themselves underinsured after an accident.

Buying the cheapest policy to satisfy the legal minimum. This keeps you legal but leaves enormous financial exposure. The minimum exists to satisfy a law — not to protect you.

Assuming liability covers everything after an accident. It covers the other person’s damages. Not yours. Many drivers genuinely don’t understand this until they’re looking at a repair bill for their own car.

Never updating coverage after life changes. You buy a home. Your income grows. Your savings increase. Your financial exposure grows with all of that — but your liability limits stay wherever you set them years ago unless you actively change them.

Not knowing about commercial exclusions. Drivers who occasionally do delivery or rideshare work on a personal policy are often completely uninsured for those trips without realising it.

Frequently Asked Questions About Auto Liability Insurance

What does auto liability insurance cover? It covers injuries and property damage you cause to other people in an accident where you’re at fault — including medical bills, lost wages, pain and suffering, and vehicle or property repairs — up to your policy limits.

Does liability insurance cover me if someone hits me? No. If someone else causes the accident, their liability insurance covers your damages. Your own liability coverage only applies when you’re at fault.

What does 100/300/100 mean in car insurance? It means your policy pays up to $100,000 per injured person, $300,000 total per accident for all injured people combined, and $100,000 for property damage.

Is liability insurance the same as full coverage? No. Liability insurance covers other people’s damages when you’re at fault. Full coverage adds protection for your own vehicle through collision and comprehensive coverage.

What happens if damages exceed my liability limits? The injured party can pursue the remaining amount from you personally — through lawsuits, wage garnishment, or asset seizure. This is why carrying adequate limits matters so much.

Does liability insurance cover rental cars? In most cases your personal liability coverage extends to rental cars you use for personal trips. It typically does not cover damage to the rental vehicle itself.

Will my insurance defend me if I get sued? Yes. If someone sues you after an accident you caused, your insurance company provides legal defense and covers costs up to your policy limits.

What if I borrow someone’s car and cause an accident? The vehicle owner’s insurance typically applies first. Your own policy may provide secondary coverage. The specifics vary by state and policy.

Does liability insurance cover parking lot accidents? Yes. If you hit another vehicle or damage property in a parking lot and you’re at fault, your property damage liability covers the repairs.

How much liability insurance do I actually need? At minimum, 100/300/100 is what most insurance professionals recommend. If you have significant assets — a home, savings, investments — higher limits or an umbrella policy are worth serious consideration.

The Bottom Line

Auto liability insurance is the foundation of every car insurance policy. Get it wrong — too little coverage, wrong limits, misunderstanding what it covers — and a single accident can create financial consequences that follow you for years.

The good news is that meaningful protection doesn’t cost as much as most people assume. Going from minimum coverage to genuinely adequate limits is often a small monthly difference for a dramatically better safety net.

Review your policy. Look at your limits. Ask yourself honestly whether they’re high enough to protect what you’ve built.

And if you’re not sure — talk to an insurance professional before you need to talk to a lawyer.