Landlord Insurance Policy

Property can accumulate wealth in the long run. Month after month the rent with which we are paying down the mortgage comes in, and the property itself has the potential to appreciate over time.

But behind that steady income is real risk. Fires happen. Pipes burst. Tenants stop paying. Visitors slip and sue.

This is where landlord insurance comes into play.

Bringing it all together: what is and what is not covered, how it differs from home insurance, cost and how to pick a policy, all in one place. Read this article completely with real life examples so that you do not take rushed decisions.

What Is a Landlord Insurance Policy?

A landlord insurance policy (also called rental property insurance or buy-to-let insurance) is designed specifically for properties that are rented out to tenants.

This is different from homeowners insurance.

As soon as you start receiving rent, your property is part of a business. That changes the risk completely. A standard home insurance policy differentiates between owner-occupied homes and rental properties. If you have a regular homeowners policy and are renting out the property, your claim can be denied.

Landlord insurance is built for situations like:

A tenant causes damage

A storm makes the property unlivable

A guest gets injured and sues you

A tenant stops paying rent

It protects the building, your income, and your legal exposure.

What Does Landlord Insurance Cover ?

Most policies are built from core sections. You can usually add optional extras depending on your needs.

1. Buildings Insurance (The Structure)

This is the foundation of any landlord policy.

It covers the physical structure of the property, including:

- Roof, walls, floors

- Fitted kitchens and bathrooms

- Built-in cupboards and fixtures

- Permanent installations like plumbing and wiring

Typical covered events include:

- Fire and smoke damage

- Storms and wind damage

- Burst pipes and water escape

- Flood (sometimes optional)

- Subsidence or ground movement

- Vandalism and malicious damage

Real example: A kitchen fire damages two rooms and part of the roof. Buildings insurance pays for repairs or rebuilding up to the insured amount.

Important: Insurance is based on rebuild cost, not market value. Rebuild cost is what it would take to reconstruct the property from scratch.

2. Contents Insurance (If Furnished)

If you rent out a furnished property, contents cover protects items you own, such as:

Furniture

White goods (fridge, washing machine, oven)

Carpets and curtains

Appliances you provided

It does not cover tenants’ personal belongings. Tenants need their own renters insurance for that.

If you rent out an unfurnished property, you may still want limited contents cover for carpets or appliances you provide.

3. Property Owner’s Liability Insurance

This is one of the most important sections.

It protects you if someone is injured and holds you legally responsible.

It can cover:

- Medical costs

- Legal fees

- Court settlements

Real example: A tenant slips on a loose stair rail that you failed to repair and breaks an arm. They sue for compensation. Liability cover pays legal expenses and settlement costs.

Most policies offer at least £1 million or $1 million in liability cover. Many experienced landlords choose higher limits because injury claims can become expensive quickly.

4. Loss of Rental Income (Loss of Rent)

If the property becomes uninhabitable due to an insured event, you cannot collect rent.

Loss of rent coverage replaces rental income for a set period, often 6 to 12 months, sometimes longer.

Real example: A major flood damages the property. Repairs take eight months. Loss of rent coverage continues paying your rental income during that time.

This is especially important if you rely on rent to pay the mortgage.

5. Rent Guarantee Insurance

This is different from loss of rent.

Loss of rent applies when the property is damaged.

Rent guarantee applies when a tenant simply stops paying.

It usually starts after a short waiting period and may cover unpaid rent for up to 12 months while legal action is taken.

This coverage became more popular after court backlogs increased eviction timelines in recent years.

6. Legal Expenses Cover

Rental disputes can become expensive.

Legal expenses coverage can help pay for:

Eviction proceedings

Recovering unpaid rent

Defending against tenant claims

Contractor disputes

A contested eviction can take months and cost thousands in legal fees. This coverage reduces that financial burden.

Condo vs Homeowners Insurance: Key Differences Explained

The Future of Insurance: How AI Is Changing Risk Assessment

What Landlord Insurance Does NOT Cover

No policy covers everything. Common exclusions include:

- Normal wear and tear

- Tenant’s personal belongings

- Intentional damage caused by the landlord

- Long-term vacant property beyond allowed limits

- Pre-existing structural defects

- Pest infestations

- Illegal activities on the property

Example: Worn carpets after five years are considered normal wear and tear, not an insured event.

Vacancy rules are especially important. Many policies only allow 30 to 60 consecutive days of vacancy before coverage changes. If the property will be empty longer, you must inform your insurer.

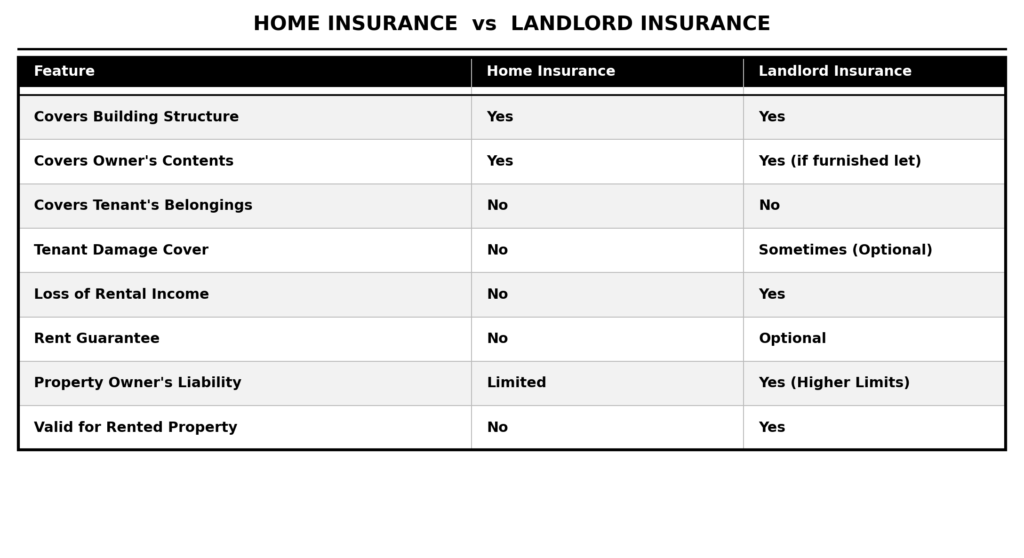

Landlord Insurance vs Home Insurance

Here is a simple comparison:

If you rent out a property under a standard homeowners policy, a claim may be rejected once the insurer discovers tenants are living there.

How Much Does Landlord Insurance Cost?

Costs vary depending on:

- Location (crime rate, flood risk, storm risk)

- Rebuild value of the property

- Type of tenants

- Number of units

- Coverage limits

- Claims history

- Optional extras

In the UK, a basic landlord buildings policy for a standard property may start around £150 to £200 per year. A more complete policy with liability, rent guarantee, and legal cover may range from £300 to £600 annually.

In the US, landlord insurance typically costs 15–25% more than standard homeowners insurance for the same property.

If you own multiple rental properties, portfolio policies can reduce the per-property cost.

How to Choose the Right Policy

First, calculate your rebuild cost accurately. Do not guess.

Second, match coverage to your tenant type. Student lets or multi-occupancy properties may require special policies.

Third, choose adequate liability limits. The cost difference between £1 million and £5 million in cover is often small.

Fourth, understand vacancy rules. If your property may sit empty between tenants, confirm how long you are covered.

Fifth, compare policies carefully. The cheapest premium may come with higher deductibles or more exclusions.

Ask clear questions about:

- Tenant damage definitions

- Accidental damage coverage

- Rent guarantee conditions

- Claim process timelines

Reading the policy wording before you need it can prevent major problems later.

Frequently Asked Questions

Q: Is landlord insurance legally required?

It isn’t legally required in most places. That said, many mortgage lenders will still ask for buildings insurance. Hypothetically speaking, running without landlord insurance is economically dangerous.

Q: Does landlord insurance cover tenant damage?

Malicious tenant damage is included with some policies. Others require an add-on. Always review your own policy wording.

Q: Can I keep my home insurance and rent out the property?

No, standard home insurance typically does not cover you for rental use. If there are tenants residing on the property, that could also lead to claims being denied.

Q: What is the difference between rent guarantee and loss of rent?

Loss of rent covers income when the property is physically damaged. Rent guarantee covers unpaid rent when tenants stop paying.

Q: Does landlord insurance cover empty property?

Yes, but this is temporary and usually for around 30–60 days. Extended absence may need special cover.

Q: Is landlord insurance tax deductible?

One of the advantages of landlord insurance is that in many countries around the world, landlord insurance premiums are deductible as a rental expense. Check with an expert in your national taxation system.

The Bottom Line

Rental property can be a powerful long-term investment. But one serious incident — a fire, lawsuit, or non-paying tenant — can wipe out years of profits.

Landlord insurance works as a safety net.

Buildings cover protects your physical asset.

Liability cover protects your personal finances.

Loss of rent protects your income stream.

Legal and rent guarantee coverage protect you from slow, costly tenant disputes.

The right policy needs to be purchased at the right timing — before any disaster strikes. It is too late when the damage is done.

You should not live your life expecting the worst to happen. It is about being ready so that the one negative thing does not destroy all the great things built over years of hard work.

Disclaimer: This article is strictly for general informational purposes and does not constitute financial or insurance advice. Additionally, the terms of coverage and the relevant laws will differ from one nation to another, and one insurer to the next. Always read the full policy wording and consult a licensed insurance professional before purchasing coverage.