Imagine this.

You are driving home from work. The light turns green. You move forward. Suddenly, another car crashes into you from the side. Your car is damaged. Your shoulder is injured. You exchange details at the scene and later call your insurance company.

A few days later, you hear something shocking: the other driver had no insurance.

At that moment, one question matters more than anything else:

Do you have uninsured motorist coverage?

Many people have heard the term. Very few truly understand what it does, what it doesn’t do, and why it can protect you from serious financial trouble. Let’s break it down in simple, real-world language.

What Is Uninsured Motorist Coverage ?

Uninsured Motorist Coverage (often called UM coverage) is part of your auto insurance policy. It protects you if someone hits you and they have no liability insurance.

Instead of chasing that driver for money — which usually means trying to collect from someone who doesn’t have enough money — your own insurance company pays for your losses.

There are usually two parts:

- Uninsured Motorist Bodily Injury (UMBI) – Covers medical bills, lost wages, and pain and suffering for you and your passengers.

- Uninsured Motorist Property Damage (UMPD) – Covers damage to your car caused by an uninsured driver.

Some states require both. Some require only bodily injury. Some don’t require either but make insurers offer it.

The key idea is simple: this coverage protects you from other people’s mistakes and irresponsibility.

What About Underinsured Motorist Coverage ?

Uninsured motorist coverage is often sold together with Underinsured Motorist Coverage (UIM).

Here’s the difference in plain English:

- Uninsured = The other driver has no insurance.

- Underinsured = The other driver has insurance, but not enough.

Let’s use a real-life example.

A driver hits you and carries only $25,000 in liability coverage (which is the minimum in many states). But your total medical bills, lost income, and therapy cost $90,000.

Their insurance pays $25,000 — and stops.

Your underinsured motorist coverage can then pay the remaining amount (up to your policy limit).

In reality, minimum insurance and no insurance create the same problem: you don’t get fully paid. That’s why UM and UIM usually come together.

How Big Is the Problem ?

Many people think, “This probably won’t happen to me.”

But statistics tell a different story.

According to the Insurance Research Council, about 1 in 8 drivers in the United States is uninsured. In some states, the number is even higher.

Think about that.

If you pass 100 cars on the highway, around 12 of them may not have insurance at all.

And accidents are expensive. Even a moderate injury can cost tens of thousands of dollars. A serious accident with surgery or long recovery can easily reach six figures.

Without UM or UIM coverage, you may be left covering those costs yourself.

Motorcycle Courier Insurance: Must-Have Cover for Riders

What Does Uninsured Motorist Coverage Pay For ?

This is where many people underestimate its value.

1. Medical Expenses

Hospital visits, surgery, X-rays, physical therapy, medications, and follow-up appointments are covered under UMBI.

Example:

You break your leg in an accident caused by an uninsured driver. Surgery and rehab cost $35,000. UMBI helps pay those bills.

2. Lost Wages

If you cannot work for weeks or months, UMBI can pay for your lost income.

Example:

A delivery driver misses two months of work due to back injuries. That lost income can be covered.

3. Pain and Suffering

Health insurance does not pay for emotional distress or physical pain. UMBI does.

This often becomes one of the largest parts of serious claims.

4. Funeral Costs

In fatal accidents, UMBI can help cover funeral expenses.

5. Car Repairs

UMPD pays to repair or replace your vehicle if an uninsured driver damages it.

Sometimes collision coverage may also apply, but collision usually has a deductible. In some states, UMPD may not.

6. Hit-and-Run Accidents

In most states, uninsured motorist coverage also applies to hit-and-run crashes.

If someone hits your car and drives away, UM coverage can step in.

What It Does NOT Cover

It’s equally important to understand the limits.

Uninsured motorist coverage does not apply if you caused the accident.

It usually does not cover damage to other property like fences or buildings.

Underinsured coverage does not stack automatically in every state. If you have $100,000 in UIM and the other driver pays $25,000, you may only receive the difference up to your limit — not an extra $100,000.

Rules vary by state and policy.

Is It Required by Law ?

Some states require uninsured motorist bodily injury coverage. Others only require insurers to offer it. Some states make it optional.

Even in states where it is not required, declining it can be risky.

Just because something is optional does not mean it is unnecessary.

How Much Coverage Should You Carry ?

A smart rule is simple:

Match your UM/UIM limits to your liability limits.

If you carry:

$100,000 per person / $300,000 per accident in liability coverage

Then carry the same for UM/UIM.

Here’s why.

If you believe $100,000 is enough to protect someone else from injuries you cause, your own body and income deserve the same protection.

State minimums are often too low. A $25,000 minimum sounds decent — until you see one hospital bill.

How a Claim Works in Real Life

This surprises many people:

When you file a UM claim, you are filing against your own insurance company.

That means the company may review your injuries carefully, question documentation, and negotiate the settlement.

You should:

- Call police at the accident scene

- Get a copy of the police report

- Seek medical care immediately

- Keep all medical bills and records

- Document missed work

In larger injury cases, many people consult a personal injury attorney.

Most UM disputes are resolved through negotiation or arbitration.

Understanding Stacking

If you own multiple vehicles, stacking may apply.

Example:

You own two cars, each with $100,000 in UM coverage. If stacking is allowed in your state and policy, you might access $200,000 total for one serious injury claim.

Not all states allow stacking. Not all policies include it.

If you have multiple vehicles, it’s worth asking your agent directly.

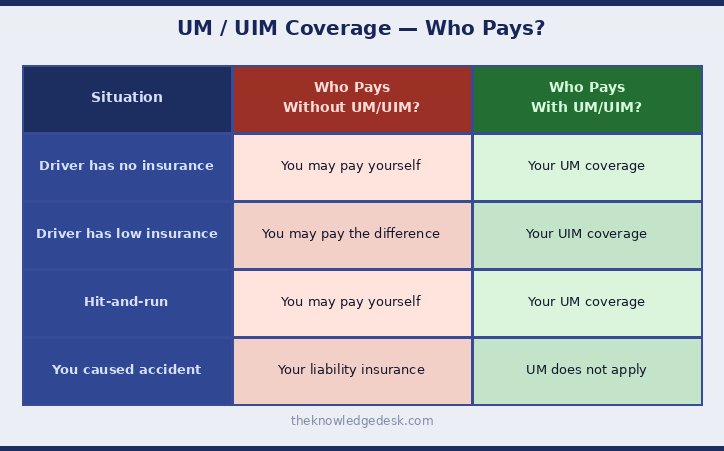

Quick Comparison Table

Here’s a simple table to understand the difference:

Frequently Asked Questions

Is uninsured motorist coverage worth it?

For most drivers, yes. It is usually affordable compared to the protection it provides.

Does it cover hit-and-run accidents?

In most states, yes.

Can health insurance replace it?

No. Health insurance pays medical bills only. It does not cover lost wages, pain and suffering, or vehicle damage.

Will filing a claim raise my rates?

It depends on your state and insurer. Some states prevent rate increases for not-at-fault accidents.

Is “full coverage” enough?

“Full coverage” usually means liability, collision, and comprehensive. It does not automatically include UM/UIM. Always check your policy.

The Bottom Line

The insurance system works well — but only when the at-fault driver has insurance.

When they don’t, uninsured and underinsured motorist coverage becomes your financial safety net.

It protects your health, your income, and your savings from someone else’s mistake.

The cost to add or increase UM/UIM coverage is usually small. The protection can be life-changing.

Before you need it, open your policy. Look at your UM/UIM limits. If they are at the minimum, consider raising them.

This is one decision that feels expensive before an accident — and obvious after one.