Key Takeaways:

- Any business that makes, imports, or sells a physical product can be sued — not just manufacturers

- You can be sued even if you did nothing wrong — legal defense alone can cost $50,000+

- U.S. law holds businesses strictly liable for defective products, even without negligence

- Small business policies start at around $200 to $600 per year for low-risk products

- Product recalls are NOT covered — that requires a separate policy

- Amazon and other platforms now require proof of coverage above certain sales thresholds

Product liability insurance is a type of business insurance that protects you when a customer claims your product caused them injury, illness, or property damage. It covers your legal defense costs, settlements, court-ordered compensation, and medical bills — regardless of whether the claim is legitimate or not.

In the United States, where strict liability laws mean businesses can be held responsible even without negligence, product liability insurance is one of the most critical protections any seller of physical products can carry.

Introduction: One Customer. One Claim. Everything Gone.

Let’s say you sell something simple. A kitchen gadget. A kids’ toy. A face cream. A phone charger you sourced from Alibaba and started selling on Amazon.

Everything is going fine — until one customer says your product hurt them.

Now you have a lawsuit. And if you don’t have product liability insurance, that single claim could wipe out everything you’ve spent years building.

This is not a scare tactic. It happens to small businesses every single day in the United States — to sellers who thought they were too small, too careful, or too new to worry about it.

What Is Product Liability Insurance?

It’s insurance that protects your business when someone claims your product hurt them, made them sick, or damaged their property.

Notice the word claims — not proved. You can be dragged into a lawsuit even if you did absolutely nothing wrong. And even if you win in court, your legal bills can easily hit $50,000 or more just from fighting the case.

Product liability insurance steps in and covers your lawyer fees and court costs, any settlements you agree to pay, compensation a court orders you to pay, and medical bills if someone was injured by your product.

In most cases the insurance company also handles finding lawyers and negotiating on your behalf. You don’t have to figure it all out alone while also trying to run a business.

Why This Matters More in America Than Anywhere Else

The U.S. legal system is uniquely aggressive when it comes to product claims. Juries can award enormous amounts. Lawyers take product injury cases on contingency — meaning they only get paid when you lose — so they’re financially motivated to pursue cases hard.

There’s also something called strict liability in American product law. In plain English: even if you didn’t do anything deliberately wrong, you can still be held responsible for a defective product. You don’t have to be careless. The product just has to cause harm.

That one legal principle is why so many businesses get completely blindsided. They assumed that because they didn’t do anything wrong, they couldn’t be held responsible. That’s not how it works here.

Who Actually Needs Product Liability Insurance ?

Most people assume it’s only for large manufacturers. It isn’t. If you’re anywhere in the chain between making a product and a customer buying it, you could be named in a lawsuit.

Manufacturers are the obvious example. If you make it and it hurts someone, you’re liable.

Importers are often surprised by this one. If you bring products in from China or anywhere overseas and sell them in the U.S., American law can treat you as the manufacturer — even if you never touched the production process, never visited the factory, never made a single design decision.

Online sellers selling on Amazon, Etsy, Shopify, or their own websites are exposed. The same platform that gets your product in front of customers nationwide also puts you in front of potential plaintiffs nationwide.

Private label sellers face significant exposure. If you’re putting your brand name on a product someone else manufactured, customers see your name. Lawsuits follow your name — not the factory’s name on the other side of the world.

The explosion of e-commerce has pulled millions of small sellers into product liability territory. Most of them genuinely have no idea.

What Types of Problems Lead to Product Liability Claims ?

There are three main ways products cause harm — and trigger lawsuits.

Manufacturing defects happen when something goes wrong during production. The design was fine, but a bad batch came through — wrong materials, poor assembly, a component that wasn’t tested properly. One bad production run hits the market and suddenly you have injured customers.

Design defects are more serious because the problem exists in every single unit. A ladder that tips too easily. A baby carrier with a weak clip. If the design itself is dangerous, the entire product line carries the same risk.

Failure to warn is the one that catches people most off guard. A cleaning product that causes burns if mixed with another common household chemical — but the label doesn’t say that. A power tool sold without proper safety instructions. You can be sued not for what the product does, but for what you failed to tell people about it.

All three types are covered under a standard product liability policy.

What Does Product Liability Insurance Actually Cover ?

A standard policy covers four main areas.

Medical costs — hospital bills, rehabilitation, lost wages during recovery, and compensation for pain and suffering if someone is injured using your product.

Property damage — your charger starts a fire in a customer’s apartment. Your appliance leaks and destroys their hardwood floor. The damage to their home or belongings is covered.

Legal defense — even if a claim is completely fabricated, you still need lawyers to prove that. The insurance pays for your defense whether you’re ultimately found liable or not.

Wrongful death — if someone dies as a result of a product defect, their family can file suit. These cases often result in the largest payouts. A solid policy covers this too.

What Product Liability Insurance Does NOT Cover

These exclusions catch businesses off guard regularly.

Product recalls are not covered. If you need to pull 10,000 units off shelves, the cost of collecting, replacing, and communicating that recall is not covered by product liability insurance. You need a completely separate product recall policy.

Employee injuries fall under workers’ compensation, not product liability.

Intentional wrongdoing voids your coverage. If evidence shows you knew the product was unsafe and sold it anyway, insurers will deny the claim.

Pure financial loss without injury — if your product simply doesn’t work as advertised and a customer wants their money back, but nobody was hurt and nothing was damaged, standard policies typically don’t cover that.

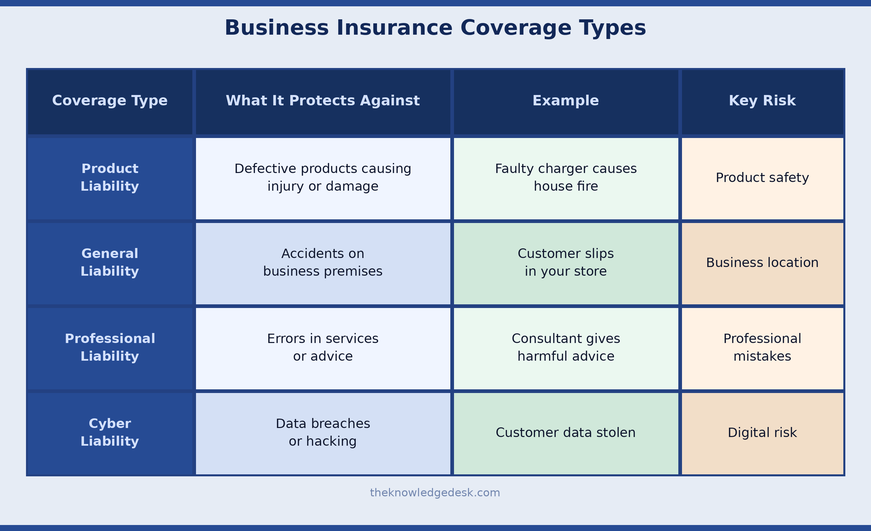

Product Liability vs Other Business Insurance

Cyber Liability Insurance: What It Covers & Why It Matters

Professional Liability Insurance: What It Is, What It Covers

Many U.S. businesses combine product liability with general liability under a Commercial General Liability (CGL) policy. Many small business owners don’t realise it’s in there — or don’t know whether the limits are high enough for what they actually sell.

How Much Does Product Liability Insurance Cost ?

Cost depends primarily on what you sell and how much of it you sell.

Low-risk products — clothing, home decor, simple tools — typically cost $200 to $600 per year for a small business when bundled with general liability coverage.

Higher-risk products — electronics, supplements, skincare, children’s products — cost more. Expect $1,000 to several thousand dollars annually depending on revenue and claims history.

Most small businesses start with $1 million in coverage. Larger companies typically carry $2 million, $5 million, or more.

The bigger your sales volume, the more products are out in the world that could potentially generate a claim. Insurers price that exposure accordingly.

Real Examples of Product Liability Claims

These aren’t worst-case scenarios. They’re ordinary situations that happened to ordinary businesses.

A small Amazon seller was offering a budget phone charger. One unit overheated overnight and caused a fire in a customer’s home. The customer sued for property damage, lost belongings, and emotional distress. Six figures to settle.

A skincare brand launched a new moisturiser. Multiple users had severe allergic reactions requiring emergency treatment. Legal costs alone before settlement exceeded $100,000 — even though the company settled relatively quickly.

A toy sold through a major retailer broke during normal play. A small piece came off. A toddler choked on it. That case went to trial.

The businesses involved weren’t reckless. They weren’t negligent in obvious ways. They just didn’t have the protection that should have been there from day one.

How to Reduce Your Product Liability Risk

Insurance covers the financial damage. But it’s far better to avoid the claim entirely.

Test properly before launch. Not a quick visual check — actual testing against relevant safety standards for your product category.

Write thorough instructions and warning labels. If there are ways to misuse your product that could cause harm, say so clearly on the label. Over-explaining protects you.

Keep manufacturing records. Know your batch numbers. Know which units shipped where. If something goes wrong, you need to be able to trace it quickly.

Vet your overseas suppliers. Ask for safety certifications. Request test reports. Don’t assume a product is safe because it arrived undamaged and looks fine.

Strong safety practices reduce claims — and many insurers will also lower your premium in response to documented quality controls.

When to Review and Update Your Coverage

Don’t buy a policy and forget it exists.

Review it once a year as standard. And revisit it specifically when you launch a new product in a different category, when your sales jump significantly, when you start selling in new states or internationally, or when a platform you sell through starts requiring proof of coverage.

Amazon now requires many third-party sellers to carry product liability insurance once they cross certain sales thresholds. Other major platforms are following the same path. Getting dropped from a platform for lack of coverage can hurt as much as a lawsuit.

Frequently Asked Questions

What is product liability insurance in simple terms? It’s insurance that pays your legal costs and any compensation owed if a customer claims your product hurt them or damaged their property — whether or not the claim turns out to be valid.

Is product liability insurance legally required in the U.S.? Not by federal law. But retailers, distributors, and major platforms like Amazon increasingly require it before they’ll work with you or allow you to sell above certain thresholds.

Who needs product liability insurance? Any business that manufactures, imports, distributes, or sells physical products — including online sellers, private label brands, and solo e-commerce operators.

Does product liability insurance cover product recalls? No. Recalls require a completely separate product recall insurance policy. This is one of the most commonly misunderstood gaps in coverage.

How much product liability insurance do I need? Most small businesses start at $1 million in coverage. If you sell higher-risk products, have significant sales volume, or sell to major retailers, consider $2 million or more.

Can a solo seller or side hustle get product liability insurance? Yes. Policies exist specifically for small sellers, home-based businesses, and solo operators. The cost for low-risk products is often very manageable.

What happens if a product liability claim is false? Your insurance still covers your legal defense costs while you fight the claim. You don’t have to prove innocence out of pocket.

Does product liability insurance cover overseas manufacturers? It covers your liability as the seller or importer in the U.S. market. It doesn’t extend to the overseas manufacturer’s liability in their own country.

What’s the difference between product liability and general liability insurance? General liability covers accidents that happen at your physical business location. Product liability covers harm caused by products you sell, regardless of where the harm occurs.

How do I get product liability insurance? Through a commercial insurance broker, directly through insurers like Hiscox, Next Insurance, or The Hartford, or through marketplace programs if you sell on platforms like Amazon that have partnered insurance options.

Final Thoughts

You can do everything right — test your product carefully, write clear labels, work with a reputable manufacturer — and still end up in a lawsuit. That’s simply how product liability works in the United States.

The insurance doesn’t stop accidents from happening. What it does is make sure that one bad claim doesn’t become a business obituary.

For anyone selling a physical product in America — whether you’re a solo Etsy seller or a growing manufacturer shipping nationwide — this coverage isn’t really optional anymore. It’s the foundation everything else sits on.

Get the coverage. Know exactly what it includes and what it excludes. Review it every year.

Then get back to building your business.