Key Takeaways:

- On a $350,000 mortgage at 6.5% over 30 years, you repay close to $800,000 total — the interest alone nearly equals what you borrowed

- Extra payments go directly to principal, immediately reducing the balance on which future interest accrues — this is where the real savings live

- Most US and UK floating-rate mortgages carry no prepayment penalties — fixed-rate deals may include early repayment charges of 1 to 5%

- Paying off your mortgage early is not automatically the right move — high-interest debt and an empty emergency fund take priority

- The psychological value of being mortgage-free is real and counts as a genuine return even when investment arithmetic might suggest otherwise

- Starting early in the loan term produces dramatically larger savings than the same payments made later

Paying off your mortgage early means making extra payments directly toward your principal — which reduces the balance faster, cuts years off your loan term, and saves a significant sum in interest — but whether it’s the right choice depends entirely on your interest rate, your other debts, your emergency reserves, and your personal tolerance for carrying debt.

The Conversation That Happens at Kitchen Tables Everywhere

One person says: we should throw everything we have at the mortgage and just be done with it.

The other says: are we sure that’s actually the smartest move?

Both instincts are reasonable. Both deserve a proper answer.

Paying off a mortgage early can save you a substantial sum in interest, eliminate a major monthly liability, and deliver a kind of peace of mind that no investment account can quite replicate. But it’s not automatically the right call for every household, every income level, or every stage of life.

This guide walks through the real mechanics, the strategies that deliver the biggest impact, and the situations where it makes more sense to redirect that money elsewhere.

Why Early Payoff Saves So Much Money

Most people understand that mortgages involve interest. The scale of it still surprises people when they actually sit down and run the numbers.

On a 30-year mortgage of $350,000 at 6.5%, the total amount repaid over the life of the loan approaches $800,000. On a £300,000 mortgage at 5% over 25 years, total repayments approach £530,000.

In both cases you’re repaying significantly more than you borrowed — and the difference is entirely interest.

The reason is amortisation. In the early years of a mortgage, the vast majority of each monthly payment goes toward interest rather than reducing the principal balance. On a standard 30-year schedule, you might be a decade in before your monthly payment splits even roughly evenly between the two.

When you make extra payments, they go directly to the principal. Reducing the principal faster means less outstanding balance on which interest accrues the following month.

That compounding effect — working in reverse and in your favour — is where the real savings come from. Even modest extra payments made consistently in the first decade can shave years off the repayment schedule and save amounts that dwarf the payments themselves.

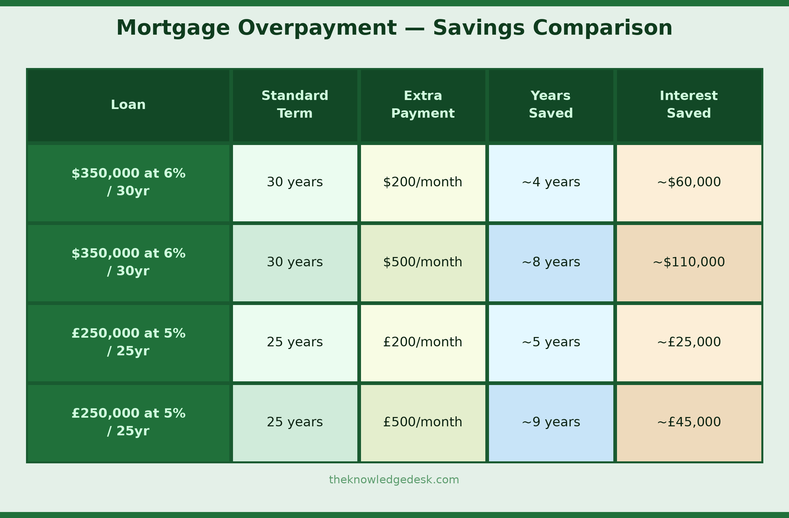

A quick example: On a $350,000 mortgage at 6% over 30 years, adding just $200 extra per month from the start shaves roughly four years off the term and saves over $60,000 in interest. On a £250,000 mortgage at 5% over 25 years, overpaying by £200 per month could cut the term by five years and save over £25,000.

The Honest Maths: What Early Repayment Actually Looks Like

The earlier you start, the more dramatic the impact. An extra $200 per month in year one does far more work than the same $200 per month starting in year fifteen — because it prevents interest from accruing on that principal for the remaining life of the loan.

Six Strategies That Actually Work

Make biweekly payments instead of monthly

Instead of making 12 monthly payments per year, pay half your mortgage payment every two weeks. The result is 26 half-payments annually — equivalent to 13 full monthly payments instead of 12. That one extra payment per year quietly eats into your principal and, over a 25 or 30-year mortgage, can shave three to five years off your term without requiring any significant lifestyle change.

In the US, check with your servicer first — some hold biweekly payments in a holding account and only credit your loan monthly, which defeats the purpose. In the UK, most lenders accept overpayments directly.

Make one extra principal payment per year

If biweekly feels complex, the simpler version is one extra full payment each year — directed specifically to principal reduction. Tax refunds, annual bonuses, and work overtime windfalls all work well for this purpose. On a 25-year mortgage, one extra payment per year can shorten the timeline by two to three years.

Always specify clearly — in writing or through your lender’s online portal — that the extra payment applies to principal. Without that instruction, some lenders apply it to future scheduled payments rather than reducing your outstanding balance.

Round up your monthly payment

If your mortgage payment is $1,847, pay $2,000. If it’s £1,250, pay £1,400. These small additions hit your principal every single month. Over years, they accumulate into a material reduction in both loan term and total interest paid — and they’re usually small enough to absorb into a budget without any meaningful sacrifice.

Apply lump sums when they arrive

Inheritance, property sales, employer bonuses, redundancy pay, stock vesting — any significant cash inflow is an opportunity for a lump sum principal payment. A single $10,000 or £8,000 lump sum prepayment in year three of your mortgage accomplishes considerably more than the same amount spread across 60 months, because it eliminates that principal immediately and prevents interest from accruing on it for the remainder of the term.

Most US mortgages and UK tracker or variable-rate mortgages carry no prepayment penalty. Fixed-rate UK mortgages typically allow overpayments of up to 10% of the outstanding balance per year before early repayment charges apply. Check your mortgage agreement before making a large lump sum payment.

Refinance to a shorter loan term.

If interest rates have dropped since you took out your mortgage, refinancing from a 30-year to a 15-year term in the US, or from a 25-year to a 15-year in the UK, can dramatically accelerate payoff.

The monthly payment increases, but the rate is typically lower, and the difference in total interest paid over the life of the loan is often substantial.

The key calculation: add up all refinancing costs — arrangement fees, legal charges, early repayment charges on the existing mortgage — and divide by the monthly savings.

That’s your break-even point in months. If you plan to stay in the property longer than that, refinancing is likely worth pursuing.

Use an offset mortgage where available.

In the UK and some parts of the US, offset mortgages allow you to link a savings account to your home loan. The balance in your savings account reduces the mortgage balance on which interest is calculated — without actually paying down the loan.

If your mortgage is £200,000 and your linked savings account holds £20,000, you only pay interest on £180,000.

You retain full access to the savings — the money is still yours to spend — but you get the interest benefit of a lower mortgage balance.

It’s particularly well suited to people with variable income who want the benefits of overpaying without locking their cash away permanently.

The Case for Paying Off Early

The arguments in favour are straightforward and the numbers are real.

You save a significant sum in interest — often more than people initially estimate. A 30-year mortgage paid off in 22 years saves eight years of compound interest accumulation, which on a large loan can run into six figures.

You free up cash flow permanently. Once the mortgage is gone, the monthly payment that previously went to the lender stays in your pocket — available for retirement contributions, travel, helping children, or simply living without that monthly obligation.

You build equity faster. Faster equity accumulation means more security and more options — remortgaging for home improvements, accessing equity if circumstances change, or having a clear-owned asset in retirement.

And the psychological dimension is real.

Research on financial wellbeing consistently shows that eliminating liabilities reduces stress and increases a sense of control, even when pure investment arithmetic might suggest the money would have grown faster elsewhere.

If being mortgage-free matters to you emotionally, that counts as a genuine return on your money.

This is especially true as retirement approaches. Entering your sixties with no housing debt significantly lowers the income you need from savings, reduces your exposure to market timing risk, and gives you considerably more flexibility about when and how you choose to work.

The Case Against Paying Off Early — When to Invest Instead

This section exists because financial decisions don’t have universal right answers.

If your mortgage carries a relatively low interest rate — say, below 5% on a fixed deal — and you have access to investment vehicles that have historically returned more than that (US index funds, global equity trackers, stocks and shares ISAs in the UK), the argument for redirecting that extra money toward investments rather than the mortgage has genuine mathematical merit.

The argument is sometimes called opportunity cost. If your mortgage costs you 4.5% in interest and a diversified equity portfolio returns an average of 7 to 10% over the long term, you’re mathematically better off investing the extra money.

But that arithmetic requires market returns to materialise — which they have historically, but not predictably year to year — and it requires you to actually invest the money consistently rather than spend it.

A guaranteed return of 5% from mortgage payoff versus a potential but uncertain return of 8% from equities is not as straightforward a comparison as the numbers suggest. Your risk tolerance, investment discipline, and time horizon all factor in.

The priority order that most financial professionals agree on:

First, pay off high-interest debt. Credit cards at 20 to 24%, personal loans at 10 to 16%, car finance — these should be cleared before accelerating mortgage payments. The interest rate differential makes this a clear priority.

Second, build an emergency fund. Three to six months of essential living expenses held in an accessible account.

Paying down your mortgage while carrying no cash reserves means any financial disruption — job loss, medical emergency, boiler replacement — could force you into expensive short-term borrowing.

Third, maximise tax-advantaged savings. In the US, maxing your 401(k) to at least the employer match and contributing to an IRA first captures guaranteed returns that mortgage payoff can’t replicate.

In the UK, using your full ISA allowance (£20,000 per year) shelters investment returns from tax in a way that often justifies prioritising it before extra mortgage payments.

After those three, the choice between extra mortgage payments and additional investment is a genuine trade-off where your specific interest rate, expected returns, tax situation, and personal preferences all influence the right answer.

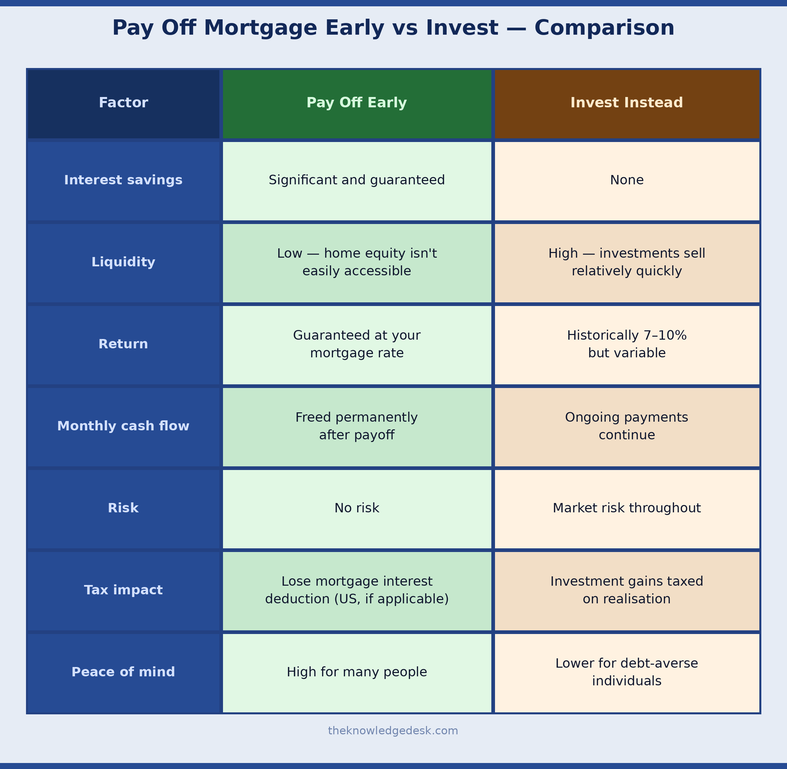

Comparison: Pay Off Early vs Invest the Difference

Tax Implications Worth Understanding

In the US: The mortgage interest deduction allows you to deduct interest paid on mortgages up to $750,000 (for loans originated after December 2017) if you itemise deductions.

Since the 2017 tax reform raised the standard deduction substantially, fewer homeowners benefit from itemising — but if you do, accelerating mortgage payoff reduces the interest you can deduct.

Paying £1 in interest to save £0.30 in tax is never a good trade, but it should factor into your effective interest rate calculation when comparing payoff against investment returns.

In the UK: There’s no mortgage interest tax relief for residential homeowners (it was phased out for buy-to-let landlords by 2020). Paying off your mortgage has no direct tax consequence for most UK residential owners, which simplifies the comparison.

However, redirecting money toward a stocks and shares ISA instead provides tax-free investment growth — worth weighing against the guaranteed return of mortgage payoff.

Always speak with a financial adviser or tax professional for guidance specific to your circumstances.

When It Makes Clear Sense to Pay Off Early

Your mortgage rate is above 6 to 7% and rising. At that level, the guaranteed return from payoff competes favourably with most investment alternatives after tax and fees.

You’re approaching retirement within five to ten years. Eliminating your mortgage payment before you stop working dramatically reduces the income your savings need to generate — and removes a significant fixed obligation from a period when income is less predictable.

You’re risk-averse or you know yourself well enough to know you wouldn’t stay invested through a market downturn.

The guaranteed return of mortgage payoff suits your temperament better than the theoretical return of equities you might sell in a panic.

You have no high-interest debt and a solid emergency fund already in place. At that point, extra mortgage payments represent one of the most reliable and predictable uses of surplus income available to you.

Mortgage Discount Points: What They Are, How They Work

When to Hold Off

Your mortgage rate is below 4 to 5% and you have the discipline to invest consistently. The mathematical case for investing the difference over a long time horizon is real.

You carry credit card balances, personal loan debt, or any other borrowing above 8 to 10%. Clear those first — the interest rate differential makes this the priority without question.

Your emergency fund is thin or nonexistent. Build that first. Mortgage prepayments are irreversible — you can’t easily pull that equity back out in an emergency without refinancing.

You haven’t yet maxed employer pension matching or your ISA allowance. These represent guaranteed or tax-sheltered returns that are difficult to replicate elsewhere.

A Practical Action Plan

Pull your current mortgage statement and understand exactly how much of your monthly payment currently goes to interest versus principal. Most US servicers and UK lenders provide this online.

The number will likely surprise you.

Run the numbers on extra payments. Even an additional £100 or $150 per month is worth calculating properly.

Most lender websites offer overpayment calculators that show the term and interest savings in real time.

Check your mortgage agreement for early repayment or prepayment clauses. US variable-rate mortgages generally carry no prepayment penalties.

UK fixed-rate deals typically allow up to 10% overpayment per year before charges apply.

If you decide to proceed, set up automatic overpayments where possible. Automation removes the temptation to redirect that money elsewhere when other spending priorities compete for it.

Review the strategy annually. As income grows or interest rates change, the balance between overpaying the mortgage and investing the difference may shift. A decision that makes sense at 6.5% may look different at 4.5% two years later.

8 Smart Ways to Get the Lowest Mortgage Rates in 2026

Frequently Asked Questions

Does paying off my mortgage early hurt my credit score?

Honestly, yes — but barely. Closing any long-standing account causes a small, temporary dip. If you have other active credit accounts in good shape, you’ll likely never notice it. Don’t let a minor score blip stop you from becoming debt-free.

What’s the difference between overpaying and paying it off completely?

Overpaying means throwing extra money at your mortgage each month while keeping the account open. Full early repayment means paying the whole thing off and closing it out. Most people are overpaying, not handing over a lump sum — and that’s completely fine.

Should I pay off my mortgage or put the money in investments?

Clear your high-interest debt first, build an emergency fund, then max out any tax-advantaged accounts. After that, compare your mortgage rate to expected investment returns. If your rate is 6.5% and markets return 8–10% long-term, investing makes mathematical sense — but only if you won’t panic-sell during a crash. If you would, just pay off the mortgage.

Will my lender charge me for paying it off early?

In the US, most standard mortgages have no prepayment penalty — but check your loan documents to be sure. In the UK, fixed-rate deals usually let you overpay up to 10% of your balance per year before charges kick in. Tracker and variable-rate mortgages typically have no restrictions at all.

How much do I actually save by making one extra payment a year?

On a $350,000 mortgage at 6.5% over 30 years, one extra payment annually knocks off roughly 3–4 years and saves $50,000–$70,000 in interest. On a £250,000 mortgage at 5% over 25 years, you’re looking at 2–3 years and £15,000–£20,000 saved. Start early — the sooner you begin, the bigger the payoff.

My income is unpredictable. Can I still pay it off faster?

Irregular income is actually perfect for lump-sum overpayments. Skip the pressure of higher monthly commitments and just dump extra money onto the principal when you have a strong month, land a big client, or receive a bonus. Your minimum payment stays manageable, but your balance still drops fast.

Does the mortgage interest tax deduction make early payoff a bad idea?

For most people, no. Since 2017, the higher standard deduction means the majority of borrowers don’t itemize anyway — so the deduction is irrelevant to them. If you do itemize and it genuinely benefits you, factor it into your rate calculation. But deliberately paying more interest just to get a deduction rarely makes financial sense.

The Bottom Line

Nobody regrets paying off their mortgage. The question is always whether the money used to do it had a better home somewhere else first.

The mechanics are straightforward — extra payments reduce principal, lower interest accrual, and compound into significant savings over time. The strategies are accessible at almost any income level. And starting earlier produces results that urgency applied later simply cannot replicate.

What isn’t straightforward is the trade-off. Your mortgage rate, your other debts, your emergency reserves, your investment options, your tax situation, and honestly how much sleep you lose over carrying debt — all of these shape the right answer for your specific situation.

Run your numbers. Check your mortgage agreement. Clear high-interest debt and build your emergency fund first. Then make the choice that fits your financial picture — not the one that makes the best headline.

Strong bones are worth building toward. So is a mortgage-free future. Both require starting earlier rather than later.

This article is for general informational purposes only and does not constitute financial advice. Consult a qualified financial adviser or mortgage professional for guidance specific to your circumstances.