Key Takeaways:

- Cyber liability insurance covers the financial damage from data breaches, ransomware, hacking, and digital fraud — none of which your standard business insurance touches

- Small businesses are targeted just as often as large ones — attackers actively prefer weaker security over bigger targets

- A single cyber incident costs the average small business over $100,000 in investigation, legal, notification, and recovery costs combined

- Most small business policies cost between $1,000 and $3,000 per year — often less than a month of software subscriptions

- Insurers can and will deny claims if you haven’t maintained basic security practices like multi-factor authentication and regular backups

- Cyber insurance covers the financial recovery — it does not prevent attacks, and it is not a substitute for proper cybersecurity

Cyber liability insurance is business insurance that pays the investigation costs, legal fees, lost income, regulatory fines, and recovery expenses that follow a cyberattack or data breach — financial damage that your existing business insurance almost certainly won’t cover.

Let me paint you a picture.

You show up to work on a perfectly normal Wednesday morning. You grab your coffee, sit down at your desk, and try to open your files.

Nothing loads.

A message appears on your screen. It tells you that all your data has been encrypted and that you need to pay a significant sum of money to get it back. Meanwhile — and this is the part that really stings — your customers’ personal information may already be sitting on a dark web marketplace somewhere.

This isn’t something that only happens to giant corporations with hundreds of employees. It happens to small restaurants. To independent law firms. To family-run e-commerce businesses. To dental practices and marketing agencies and independent consultants.

And when it happens without cyber liability insurance in place, the financial damage can be enough to close the business permanently.

That’s what this article is about — what cyber liability insurance actually is, what it covers, what it doesn’t, how much it costs, and whether your business genuinely needs it.

First, Let’s Talk About the Gap Nobody Tells You About

Most business owners assume their existing insurance covers them if something goes wrong digitally. It almost certainly doesn’t.

Your property insurance covers physical damage — fire, flood, theft of equipment. Your general liability insurance covers things like a customer slipping and injuring themselves on your premises.

Neither of them covers a hacker breaking into your system and stealing customer credit card data. Neither covers ransomware locking up your files. Neither covers the $80,000 in investigation fees, legal costs, and customer notifications that follow a data breach.

That gap is exactly what cyber liability insurance was created to fill.

So What Exactly Is Cyber Liability Insurance ?

In plain English — it’s insurance that protects your business financially when something goes wrong in the digital world.

Cyberattack. Data breach. Ransomware. An employee clicking a dodgy link and accidentally letting someone into your system. A fraudulent email that tricks your accounts team into wiring money to a criminal.

These are the scenarios cyber insurance is built for.

Most good policies cover two categories of loss:

Losses your business suffers directly — the cost of recovering your data, getting your systems back online, investigating what happened, and notifying affected customers.

Claims made against your business by others — if customers, partners, or regulators come after you because their data was compromised, the policy covers your legal costs and any settlements.

Many comprehensive policies bundle both into one package.

What Does It Actually Pay For ?

This is the part most people want to know — so let’s go through it properly.

Dealing with a data breach

When customer data gets exposed, the clock starts ticking immediately. Most states have laws requiring you to notify every affected customer within a specific timeframe. You need cybersecurity experts to investigate how it happened. You may need to offer credit monitoring services to affected customers. You’ll almost certainly need legal advice.

All of that costs money. A lot of it. Cyber insurance covers the whole response — forensic investigators, customer notifications, credit monitoring, legal consultation, and PR support to manage the reputational damage.

Lost income while you’re down

If an attack takes your systems offline, your revenue goes with them. An e-commerce store that can’t process orders. A clinic that can’t access patient records. A logistics company that can’t coordinate deliveries.

Every hour of downtime has a real cost. Cyber insurance compensates you for the income lost during recovery and can also cover emergency IT costs to get you back up and running faster.

Ransomware — the big one right now

Ransomware attacks have exploded in recent years and they show no sign of slowing down. Hackers encrypt your files and demand payment — sometimes thousands, sometimes hundreds of thousands of dollars — to hand back the decryption key.

Cyber policies typically cover professional ransom negotiators, the payment itself where it’s legally permitted, the technical work of recovering your data, and restoring your systems. Some businesses find that paying the ransom is genuinely cheaper than rebuilding from scratch — and having insurance means you’re making that decision calmly with professional support rather than in a blind panic at midnight.

Legal costs and regulatory fines

A data breach doesn’t just create a technical problem. It creates a legal problem.

Customers can sue you. Regulators can investigate and fine you — especially if you handle health information, financial data, or data belonging to European customers under GDPR. Those fines aren’t small.

Cyber insurance covers your legal defense, any court settlements, regulatory fines, and compliance investigation costs. Without it, the legal fallout from a single incident can wipe out years of profit.

Figuring out what actually happened

After any serious cyber incident, you need forensic cybersecurity specialists to trace exactly how the attack happened, what was accessed, and what you need to do to prevent it happening again.

This isn’t optional — it’s legally required in many cases, and you genuinely need to know the answers. These investigations can cost anywhere from $20,000 to well over $100,000. Most cyber policies include this as part of their standard incident response.

Getting tricked by a convincing email

Not every cyberattack involves sophisticated hacking. Sometimes it’s just a very convincing email.

Someone impersonates your CEO and asks an employee to urgently transfer funds. Or a fake vendor emails your accounts team with updated banking details. The money moves before anyone realises anything is wrong.

Some cyber policies now cover these social engineering and phishing fraud losses. It’s worth checking specifically whether yours does — because not all of them include it as standard.

What Does Liability Insurance Cover ? A Complete Breakdown

Real Businesses, Real Claims

These aren’t hypothetical scenarios.

A small restaurant discovered that hackers had been sitting quietly inside its payment system for weeks, harvesting customer card details. The insurance covered the forensic investigation, notifications to thousands of customers, credit monitoring services, and regulatory fines.

A regional real estate agency got hit with a denial-of-service attack that knocked its website offline for several days. No one could access listings or contact agents. The cyber policy covered lost revenue during the outage and the legal costs that followed.

A healthcare provider suffered a ransomware attack that locked patient records across multiple locations. Insurance covered the investigation and system restoration — though the reputational damage took considerably longer to recover from.

None of these businesses were reckless. None of them were obvious targets. They were just regular businesses going about their day — until they weren’t.

What Cyber Insurance Won’t Cover

Just as important as what it covers — here’s what it doesn’t.

Security problems you knew about and ignored. If you had a known vulnerability that never got fixed and attackers walked straight through it, your insurer may deny the claim. This is becoming more common as insurers get smarter about security assessments.

Nation-state attacks. Cyberattacks attributed to foreign governments are typically excluded. For most small businesses this is unlikely to be relevant — but it’s worth knowing.

Employees who deliberately cause a breach. Accidental mistakes by staff are usually covered. Deliberate insider wrongdoing typically isn’t.

Infrastructure failures. A power outage or broad internet failure that wasn’t a targeted attack on your business usually falls outside the policy.

Not keeping up basic security. This is the one that catches people out most often right now. Many insurers require businesses to have multi-factor authentication, regular software updates, secure data backups, and employee security training in place. If you don’t have these basics and suffer a breach, your claim could be denied outright.

The message here is simple — read the policy, understand what’s required of you, and actually do those things.

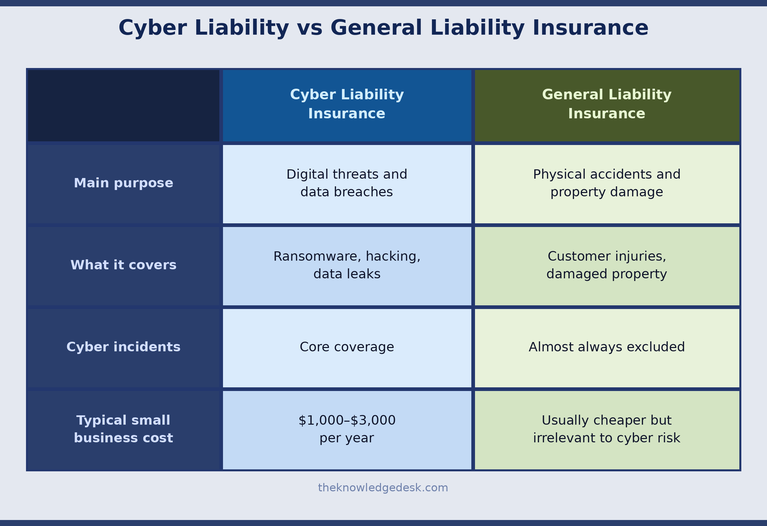

Cyber Liability Insurance vs General Liability Insurance

Here’s a simple side-by-side so you can see the difference clearly:

The short version — you need both. They cover completely different categories of risk and neither replaces the other.

Who Actually Needs This ?

Honestly? Any business that handles digital information — which in 2026 means almost every business that exists.

But some industries are at particularly high risk:

Healthcare — patient records are among the most valuable data criminals can get their hands on, and the regulatory consequences of a breach are severe.

Financial services — accountants, mortgage brokers, financial advisors, banks. High-value data and serious regulatory oversight make this a prime target.

Retail and e-commerce — payment card data, customer accounts, purchase histories. E-commerce businesses are attacked constantly because the data converts directly to money.

Law firms and professional services — confidential client information, contracts, case files. This data is valuable and law firms are increasingly targeted.

Schools and universities — large databases of student personal information and typically limited IT security budgets.

Small businesses generally — this is the one that needs saying clearly. Small businesses are often targeted because their security is weaker than larger companies. If you think you’re too small to bother attacking, that’s exactly what attackers are banking on.

Business Owner’s Policy (BOP) Insurance Explained in Simple way

Why Umbrella Insurance Might Be the Smartest $200 You Spend

What Does It Cost ?

Less than most people expect.

For small businesses, a solid cyber liability policy typically costs between $1,000 and $3,000 per year. Medium-sized businesses with more data and higher risk profiles pay more.

Your premium is influenced by:

- What industry you’re in — healthcare and finance tend to pay more

- How much sensitive data you hold and what type it is

- Your existing security practices — better security means lower premiums

- Your revenue and business size

- Whether you’ve had previous cyber incidents

- How much coverage you’re buying

Here’s the thing worth highlighting: businesses with documented, strong cybersecurity practices — multi-factor authentication, regular updates, employee training, tested backups — often pay 20 to 30 percent less than businesses without them.

Good security saves you money on insurance. That’s not a small thing.

How to Pick the Right Policy

A few things to look out for when you’re shopping around:

Don’t just look at the headline coverage number. A policy might advertise $2 million in coverage but cap ransomware payments at $250,000. If ransomware is a realistic threat for your business — and it is for most — that sub-limit matters enormously.

Check what incident support looks like. Some insurers give you a 24-hour response team when something goes wrong — cybersecurity experts, lawyers, crisis communications people. Others send you a claims form and wish you luck. The difference between those two options at 3am when your systems are locked is significant.

Work with a broker who actually understands cyber risk. This is specialised enough that a generalist broker may miss important gaps in your coverage.

Be honest on the application. Insurers ask detailed questions about your security setup. Inaccurate answers don’t just affect your premium — they can void your entire policy when you try to make a claim.

One Thing Insurance Can’t Do

It cannot stop an attack from happening.

This sounds obvious but it gets lost in conversations about cyber insurance. The insurance handles the financial recovery. It is not the prevention.

You still need patched software. Strong passwords and multi-factor authentication. Employees who know how to spot a phishing email. Regular backups that are actually tested. A basic plan for what to do if something goes wrong.

Think of it like fire insurance — you still fit smoke detectors, maintain your wiring, and train staff on fire procedures. Insurance is the backstop when prevention isn’t enough. It is not a replacement for prevention.

The businesses that recover fastest from cyber incidents are the ones that combined decent security with proper insurance coverage. The businesses that recover worst are the ones that treated insurance as a substitute for security — or didn’t have either.

Quick Answers to Common Questions

Is cyber insurance legally required? Not by most laws, though some contracts and supplier agreements require it. That’s becoming more common.

Will my existing business insurance cover a cyberattack? Almost certainly not. Most policies explicitly exclude it. Check your policy wording — don’t assume.

Does it cover ransomware payments? Many policies do, though insurer approval may be required first. Check for sub-limits on ransomware specifically.

Can I afford it as a small business? Most likely yes. Entry-level coverage can start below $1,000 per year. One serious incident without coverage can cost $100,000 or more. The maths works out.

What do I do the moment I discover an attack? Call your insurer immediately — most cyber policies have an emergency response line. Don’t wipe systems or try to fix things yourself before specialists have preserved evidence. Contain what you can, document what you see, and let the response team take over.

Will my premium increase after a claim? Almost certainly at renewal, yes. That’s standard across all insurance. It’s still worth claiming — paying out of pocket is almost always worse.

The Bottom Line

Cyber threats are not going away. If anything, they’re becoming more common, more sophisticated, and more expensive to recover from.

For most businesses, a serious cyber incident without insurance coverage isn’t just an expensive problem. It’s potentially the thing that ends the business.

For somewhere between $1,000 and $3,000 a year — often less than you spend on software subscriptions — you can make sure that a bad day in the digital world doesn’t become the worst day your business ever had.

Get the coverage. Keep up the security practices that come with it. Read the policy so you know what it actually covers.

And then get back to running your business.