A home purchase is the biggest financial decision most people will ever make. It’s exciting, emotional and full of hope — but it’s also a long‑term commitment that could impact your money for the next 15 to 30 years.

Many buyers rush through the loan process because they’re focused on getting the keys. Months down the line, this excitement often gives way to stress when EMIs start to feel burdensome or hidden costs come along for the ride.

I have seen that happen to friends, family and even financially smart people. The issue is not typically income or ambition. It’s minor missteps taken at the beginning that silently blossom into expensive mistakes over time. The good news is that avoiding most home loan mistakes is easy when you know what to look for.

This guide combines real borrower experiences, lender insights, and practical lessons into one clear explanation.

Why Home Loans Go Wrong for Many Buyers

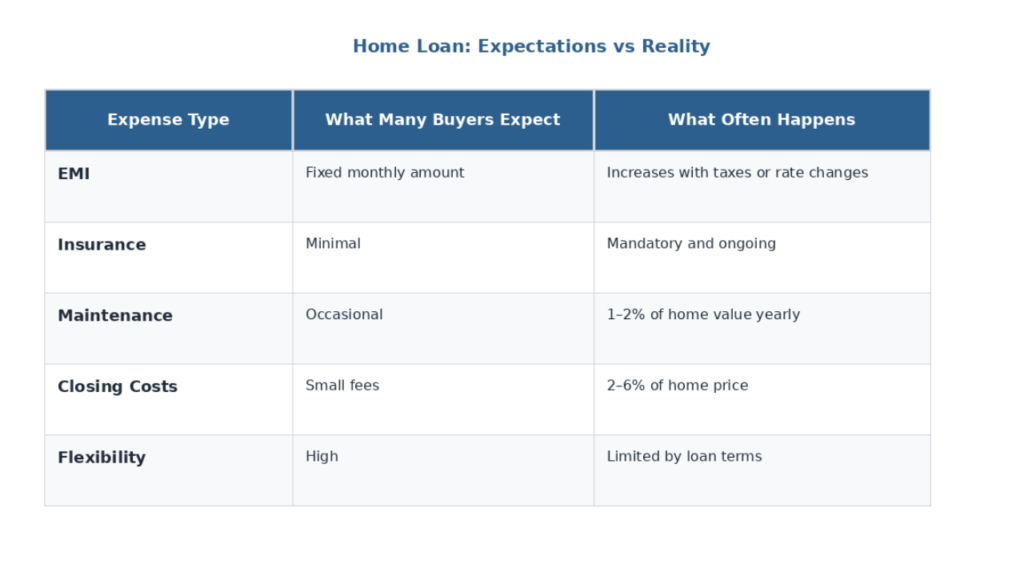

A house loan is not just about a monthly EMI. It covers interest, taxes, insurance, maintenance and fees as well as the long‑term obligations that many buyers don’t factor into their costs.

In many cases, the true cost of owning a home ends up being 40–50% higher than what people originally expect.

Lenders approve loans based on numbers, not your future life changes. They don’t take into account medical expenses or career breaks or children or emergencies. That’s why preparation matters more than speed.

Let’s take a look at some of the most common mess-ups — and how not to fall into them.

Mistake 1: Not Checking Your Credit Early Enough

Your credit score quietly controls your home loan. Many buyers only check it when they’re ready to apply, and by then, fixing issues is difficult.

Lenders usually look at credit reports from major bureaus and focus on your middle score. A score above 740 typically qualifies for the best interest rates. Scores between 650 and 739 are acceptable but cost more in interest. Below 620, options become limited and expensive.

Errors are common. Late payments that weren’t late, accounts that aren’t yours, or outdated balances can drag your score down. Fixing these takes time, often 30 to 60 days per correction.

A real example: one buyer improved his score from 680 to 760 in four months by paying down credit cards and disputing errors. That improvement saved him thousands over the loan term.

Start checking your credit at least six months before applying. Pay bills on time, keep card usage low, and avoid new loans during this period.

Mistake 2: Skipping Pre‑Approval Before House Hunting

Looking at homes without pre‑approval is like shopping without knowing your budget. In competitive markets, sellers often ignore offers that aren’t pre‑approved.

Pre‑approval shows how much you can realistically borrow and locks in a rate for a short period It also guards against falling in love with homes you can’t afford.

Yes, pre‑approval requires documents and a credit check, but it provides clarity and confidence. It also gives you leverage when you negotiate.

Mistake 3: Not Shopping Around for Lenders

Many borrowers just take the first loan package offered to them, generally from their bank. That one decision can wind up costing tens of thousands over the years.

Interest rates often vary by 0.5% or more between lenders. On a long‑term loan, that difference adds up fast. Different banks also charge different fees, penalties, and insurance costs.

Comparing lenders doesn’t hurt your credit if done within a short window. Mortgage brokers, credit unions, online institutions and big banks all have something to offer.

And borrowers who compare at least three lenders save hundreds to thousands a year, according to industry data.

Best Personal Loan Options for Low-Income Borrowers

Mistake 4: Borrowing the Maximum Amount Allowed

Just because a lender approves a certain amount doesn’t mean you should borrow it. Banks may allow EMIs up to 50–60% of income, but living that way leaves no breathing room.

Financially safer households usually keep EMIs under 35–40% of take‑home income. This allows room for savings, emergencies, and normal life expenses.

If you borrow the maximum, even a small increase in expenses can cause stress. Choosing a slightly smaller home often leads to better sleep and long‑term stability.

Mistake 5: Underestimating Down Payment and PMI Costs

Low down payment options sound attractive, but they often come with hidden costs. Putting less than 20% down usually triggers private mortgage insurance (PMI), which can add a significant monthly amount.

For a down payment, many buyers are cleaning out their savings without leaving anything for emergencies, repairs and closing costs.

A higher down payment reduces loan size, EMI, interest paid, and sometimes eliminates PMI altogether. But gift funds and assistance programs can also be game changers if they are planned correctly.

Master Mortgages, Loans & Financial Freedom – Detailed guide

Mistake 6: Ignoring Closing Costs and Hidden Fees

The purchase price is not the amount you ultimately pay. Closing costs can vary from 2-6% of the home value, which could cover processing fees, appraisals, legal checks and insurance.

Some lenders lower interest rates but increase fees. Others do the opposite. Without comparing total costs, it’s easy to choose the wrong deal.

Be sure to read the loan estimate and final disclosure carefully. Small fees add up quickly.

Mistake 7: Not Reading the Fine Print

Loan agreements are long, boring and important. They contain rules on missed payments, insurance requirements, prepayment penalties and property usage.

Some loans restrict renting the property. Others charge penalties for early repayment. Adjustable rates may rise sharply later.

If something feels ambiguous, try asking questions or seeking help from a professional. One of the most costly errors that buyers make is signing without knowing what they are signing.

Best Banking Apps That Help You Manage Loans Easily

Real Cost of Homeownership at a Glance

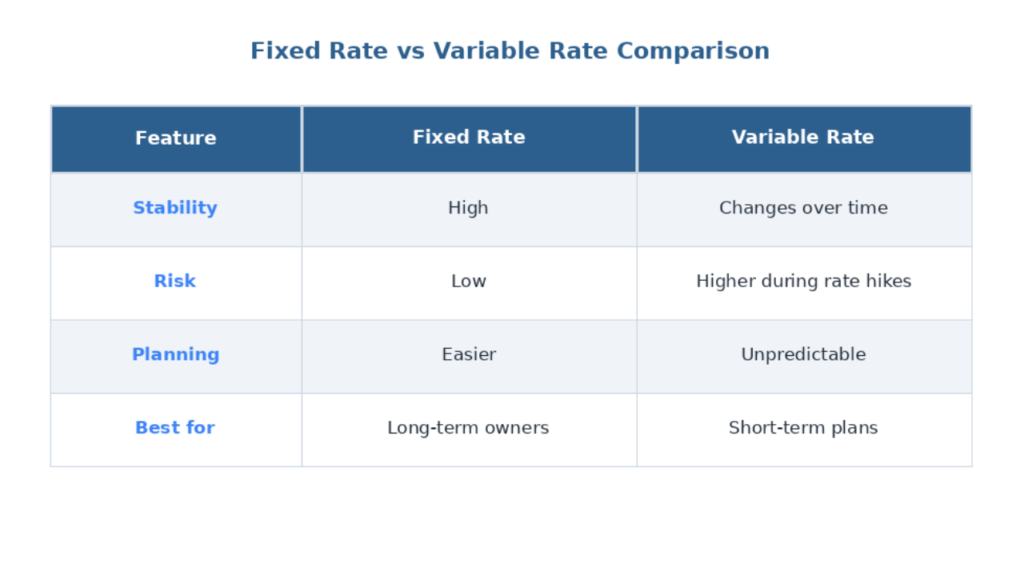

Fixed vs Variable Interest Rates (Simple Comparison)

Moving Forward With Confidence

Buying a home doesn’t need to be stressful. The goal isn’t just loan approval — it’s choosing a loan that supports your life instead of controlling it.

Start early. Check your credit. Compare lenders. Borrow conservatively. Read everything. When you move slowly and thoughtfully, homeownership becomes a source of comfort, not pressure.

How Digital Banking Is Changing Loan Approvals

Frequently Asked Questions

What credit score gives the best home loan rates?

Scores above 740 usually qualify for the lowest rates. Lower scores increase costs.

How much down payment is ideal?

20% avoids insurance costs, but smaller options exist with trade‑offs.

Can interest rates be negotiated?

Yes. Strong credit and competing offers improve your position.

Are closing costs negotiable?

Some are. Comparing lenders and asking questions helps reduce them.

Should I prepay my loan early?

If penalties are low and savings are stable, prepayment reduces interest.

What happens if I miss a payment?

Late fees apply and credit scores drop. Multiple misses can lead to default.

A home is a dream — but the loan behind it should be a smart decision. When you avoid these mistakes, you don’t just buy a house. You build long‑term peace of mind.