Key Takeaways:

- A HELOC is a revolving credit line secured against your home equity — you borrow what you need, repay it, and borrow again during the draw period

- Most lenders allow you to borrow up to 80 to 85% of your home’s value minus what you still owe on your mortgage

- Rates are variable and tied to the prime rate — currently running 7.5% to 10% in the US as of 2026

- The draw period lasts 5 to 10 years, followed by a repayment phase where payments increase significantly

- Your home is the collateral — defaulting risks foreclosure, which makes this fundamentally different from credit card or personal loan debt

- HELOC interest is only tax-deductible in the US if funds are used to buy, build, or substantially improve the home

A HELOC is a revolving line of credit secured against the equity in your home — giving you flexible, lower-rate access to funds you can draw, repay, and draw again — but because your home backs the debt, it’s a tool that rewards discipline and punishes misuse.

You’ve Been Building This Resource for Years Without Realising It

Every mortgage payment you make builds equity. Every year your home increases in value adds more. Quietly, without much fanfare, your property has been accumulating a financial resource most homeowners barely think about.

A HELOC — Home Equity Line of Credit — is one of the most flexible ways to access that resource. But flexibility cuts both ways. Used well, a HELOC funds a home renovation at a fraction of personal loan rates, consolidates high-interest debt intelligently, or sits unused as a financial safety net. Used carelessly, it ties your home’s title to a debt you can’t repay.

Here’s what you actually need to know.

What a HELOC Is

A HELOC is a revolving credit line secured against the equity you’ve built in your home. Think of it like a credit card — but attached to your property, with dramatically lower interest rates because the lender has real collateral backing the debt.

Unlike a personal loan or a home equity loan that gives you a lump sum upfront, a HELOC gives you a credit limit you can draw from, repay, and draw from again. You only pay interest on what you’ve actually borrowed.

The catch that matters most: because your home serves as collateral, defaulting on a HELOC is not like defaulting on a credit card. The lender has a legal claim on your property. That single fact deserves more weight than it typically gets in conversations about accessing home equity.

How Your Credit Limit Gets Calculated

Lenders use something called the combined loan-to-value ratio (CLTV) to determine how much they’ll lend.

Here’s how it works in practice. Your home is worth $500,000. You owe $280,000 on your mortgage. Your equity is $220,000. Most lenders allow a CLTV of up to 85%, which means they’ll lend against up to 85% of your home’s value — $425,000. Subtract your existing mortgage and your maximum HELOC is $145,000.

Most lenders cap at 80 to 85% CLTV. Your actual approved limit depends on credit score, income, and debt-to-income ratio on top of that.

The Two Phases — and Why Phase Two Catches People Off Guard

Draw period (5 to 10 years): You borrow what you need, repay it, borrow again. Monthly payments during this phase typically cover interest only on your outstanding balance — which keeps payments low and manageable.

Repayment period (10 to 20 years): The line closes. No more borrowing. Your payment now covers both principal and interest on whatever balance remains. If you spent freely during the draw period without reducing the principal, this payment jump — sometimes called payment shock — hits hard.

The smart approach: treat the draw period as if repayment has already started. Voluntarily paying down principal during the draw phase eliminates the shock entirely when the repayment phase arrives.

Interest Rates — What You’re Actually Paying

Most HELOCs carry variable rates tied to the prime rate. As of early 2026, HELOC rates in the US generally run 7.5% to 10% depending on your credit profile and lender.

Compare that to personal loans at 10 to 16%, or credit cards at 20 to 28%, and the cost advantage of a HELOC becomes obvious for borrowers with solid equity and good credit.

Some lenders offer fixed-rate conversion options — letting you lock a portion of your outstanding balance at a fixed rate during the draw period. Worth asking about if rates are rising and you want predictability on part of your debt.

HELOC Calculator

Estimate your home equity line of credit limit, monthly payments, and total borrowing costs.

Loan Terms

Fill in your home details

and hit Calculate to see

your HELOC breakdown.

Phase Breakdown

This calculator provides estimates for informational purposes only and does not constitute financial advice. Actual HELOC terms vary by lender. Consult a licensed mortgage professional before making borrowing decisions.

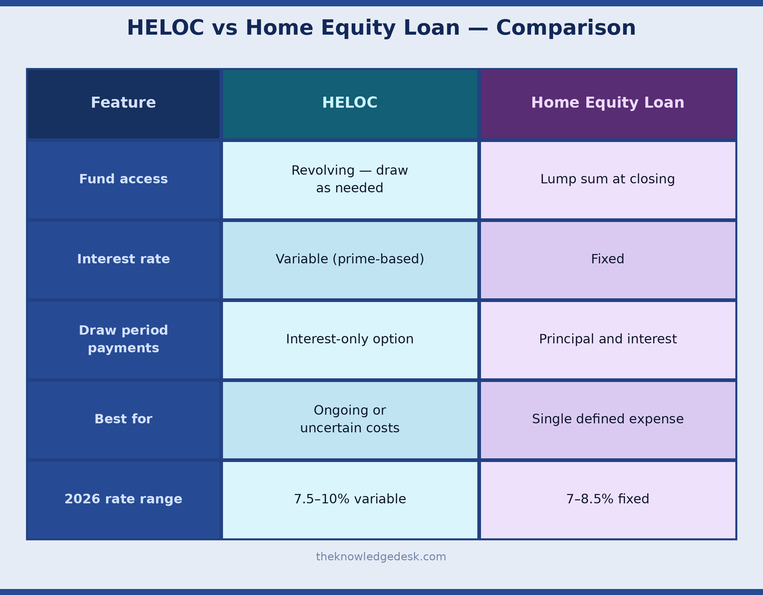

HELOC vs Home Equity Loan

The choice is straightforward. If you need money on an ongoing or unpredictable schedule — renovation phases, tuition instalments, a business with variable cash needs — the HELOC’s flexibility pays off. If you have one defined expense and want payment certainty, a home equity loan’s fixed rate is often the better fit.

Who Actually Qualifies

Lenders look at four main things.

Equity and CLTV: You need at least 15 to 20% equity remaining after the HELOC is factored in. Most lenders cap at 80 to 85% CLTV.

Credit score: Most US lenders require a minimum of 620, but 720 and above gets you the best rates. The difference between a 680 and 760 score can be 0.5 to 1% on your rate — meaningful over years of borrowing.

Debt-to-income ratio: Your total monthly debts including the HELOC payment should stay below 43 to 45% of gross monthly income.

Income documentation: Stable, documentable income matters. Self-employed borrowers face more scrutiny — lenders typically average two years of net taxable income from filed returns rather than using gross revenue.

Paying Off Your Mortgage Early? Read This First

Understanding Mortgage-Backed Securities: A Simple Guide

What to Use a HELOC For — and What to Avoid

Look, a HELOC actually makes sense in a handful of situations. Renovating your home is the big one — you’re borrowing against the house to make the house worth more. That’s not debt, that’s math.

Same logic applies when you’re drowning in credit card bills charging you 22% interest. Swapping that out for a HELOC at 8 or 9% isn’t risky — it’s just smarter.

Tuition costs work too, and honestly, keeping an untouched line sitting there as a rainy-day fund isn’t the worst idea either.

But people get themselves into real trouble when they start treating their home equity like an ATM. A vacation? A boat? A stock tip your brother-in-law swore was a sure thing? That’s how people end up underwater on a house they’ve spent fifteen years paying down.

And if you’re using a HELOC to cover groceries and electric bills every month, that’s not a solution — that’s a slow bleed that gets worse, not better.

Here’s the clearest example of it working the right way: somebody pulls $40,000 from their HELOC, guts their outdated kitchen, and puts in something buyers actually want. Their home appraises $55,000 higher afterward.

They took on $40,000 in debt and gained $55,000 in equity. That’s not a loan — that’s an investment with a built-in return.

The tool isn’t the problem. It’s knowing when to pick it up and when to leave it alone.

The Costs Beyond the Interest Rate

Upfront costs typically run $300 to $1,000 for application, appraisal, and title search. Some lenders charge an origination fee of 0 to 1% of the line.

Ongoing costs include annual fees of $50 to $100 to keep the line open, and potential inactivity fees if you don’t draw from the line.

Early closure fees apply if you close the HELOC within the first two to three years — often to recover origination costs the lender fronted.

Variable rate caps are essential to understand. Most HELOCs have periodic caps (how much the rate can jump per adjustment) and lifetime caps (the maximum it can ever reach). Ask for these numbers before signing anything.

The Risk That Deserves Blunt Language

A HELOC is a secured debt against your home. That’s not a formality.

If job loss, illness, divorce, or any disruption stops you from making payments, your home is at risk of foreclosure. This is fundamentally different from defaulting on a credit card, where the consequences are credit damage and collection calls. There’s no version of HELOC default where your home is not involved.

The practical implication: only use a HELOC for productive purposes, with a clear repayment plan before you draw the first dollar. Borrowing against your home because the money is available is not a financial strategy.

Is a HELOC Right for You?

It likely makes sense if you have substantial equity, a stable income, a specific productive use for the funds, and a plan for paying down principal during the draw period — not just after.

It probably doesn’t make sense if you’re in the early years of your mortgage with limited equity, carrying other high-interest debt you haven’t cleared, approaching retirement, or planning to use the line for expenses you can’t otherwise afford.

Frequently Asked Questions

What’s the difference between a HELOC and a home equity loan?

A HELOC is revolving with a variable rate — you draw what you need and repay it over time. A home equity loan delivers a fixed lump sum at a fixed rate with equal monthly payments. Different tools for different situations.

Is HELOC interest tax-deductible?

In the US, only if the funds are used to buy, build, or substantially improve the home securing the loan — a rule tightened in 2017. Using HELOC funds for debt consolidation or personal spending disqualifies the deduction. Consult a tax professional for your specific situation.

Can I get a HELOC with a 620 credit score?

Possible, but you’ll pay a higher rate. Most lenders want 680 minimum for reasonable terms and 720 or above for their best rates.

What happens to my HELOC if I sell my home?

It must be paid off at closing from sale proceeds, alongside your primary mortgage. If the sale price doesn’t cover both balances, you’re responsible for the shortfall.

Can I pay off a HELOC early?

Yes — most HELOCs carry no prepayment penalty. Paying down the principal aggressively during the draw period is exactly the right approach.

What if interest rates rise significantly?

Your payment increases with the rate. Model what your payment looks like if rates rise 2% before you draw anything. If that number is uncomfortable, either borrow less or ask your lender about fixed-rate conversion options.

How long does HELOC approval take?

Typically two to six weeks from application to funding. Some online lenders and credit unions have compressed this to under two weeks for straightforward applications.

The Bottom Line

A HELOC is one of the more powerful financial tools available to homeowners — precisely because it’s backed by an asset most people care deeply about protecting.

The lower rates are real. The flexibility is real. And the risk is real.

Used for value-adding purposes with a clear repayment plan, a HELOC makes excellent financial sense. Used as a spending tap attached to your home’s equity, it’s a liability dressed as an opportunity.

Know which one you’re dealing with before you sign.

This article is for general informational purposes only and does not constitute financial advice. Consult a qualified financial adviser for guidance specific to your circumstances.