Key Takeaways:

- Professional liability insurance — also called E&O insurance or professional indemnity — covers claims that your advice, services, or work caused a client financial harm

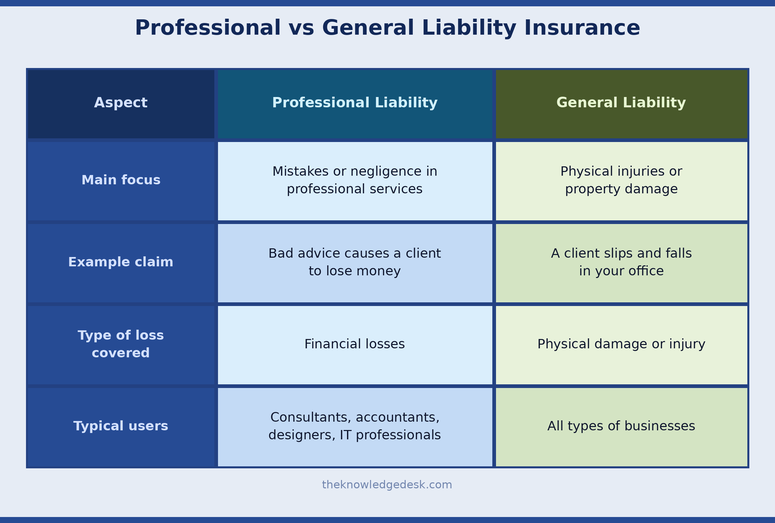

- It’s completely separate from general liability insurance — which covers physical injuries and property damage, not professional mistakes

- Legal defense alone can cost tens of thousands of dollars even when the claim is completely false — the policy covers that too

- Most policies operate on a claims-made basis — meaning the active policy when the claim is filed handles it, not the policy when the work was done

- Small business and freelancer premiums typically run $800 to $2,500 per year — a fraction of what one lawsuit costs

- Freelancers are often more exposed than larger firms because their personal assets are directly on the line

Professional liability insurance protects you when a client claims your professional advice, services, or work caused them financial loss — covering your legal defense costs, settlements, and court judgments even if the claim turns out to be completely unfounded.

The Problem With Being Good at Your Job

Here’s something nobody tells you when you start a service business.

Doing good work isn’t enough to keep you out of legal trouble.

You can be careful, experienced, and genuinely excellent at what you do — and still find yourself on the receiving end of a lawsuit. A client loses money and decides your advice was the reason. A project doesn’t deliver the results they expected. A deadline gets missed. A calculation is wrong. A detail gets overlooked.

Sometimes you made a genuine mistake. Sometimes the client’s expectations were simply unrealistic. Sometimes the lawsuit is completely without merit.

It doesn’t matter. The legal process starts either way. And without professional liability insurance, you’re paying for every bit of it yourself.

What Professional Liability Insurance Actually Is

Professional liability insurance is coverage designed for businesses that provide services, advice, or expertise. It protects you when a client claims your professional work — through error, omission, negligence, or failure to deliver — caused them financial damage.

You’ll hear it called several things depending on your industry:

Errors and Omissions (E&O) insurance — the most common term in consulting, tech, and financial services.

Professional indemnity insurance — used more often in the UK and Australia but increasingly common in the US too.

Malpractice insurance — the same concept, used specifically in medicine, law, and a few other licensed professions.

Different name, same core function — if a client comes after you professionally, this policy handles it.

How It’s Different From General Liability Insurance

This is where a lot of service business owners get caught out.

General liability insurance covers physical risks — a client slips on your floor, someone’s property gets damaged, bodily injury at your premises. It’s essential, but it covers a completely different category of risk from professional liability.

If a client walks into your office and injures themselves, general liability handles it. If a client follows your advice and loses $50,000, that’s a professional liability claim.

Most service businesses need both. They cover entirely different risks and one doesn’t substitute for the other.

What Professional Liability Insurance Covers

Legal defense costs — this is often the most immediately valuable part of the coverage. Even if a claim is completely fabricated, defending yourself costs real money. Lawyers, filings, depositions, expert witnesses — these expenses add up fast regardless of whether you did anything wrong. The policy covers your defense whether you’re ultimately found liable or not.

Settlements and court judgments — if a court rules against you or you settle a claim out of court, the policy pays up to your coverage limits. Without it, that amount comes directly from your business or personal finances.

Errors and omissions — genuine mistakes. A missed deadline, a calculation error, incomplete work, an overlooked requirement. When those errors cause financial losses for a client, the policy covers the resulting claims.

Misrepresentation or failure to deliver — clients sometimes claim you promised results you didn’t deliver, or that your services didn’t match what was described. Professional liability coverage typically handles the legal defense and damages in these situations.

Work by employees and subcontractors — most policies extend coverage to employees, partners, or contractors working on your behalf. If a subcontractor makes a mistake on your project and the client comes after you, the policy generally covers it.

Real Situations Where This Coverage Actually Matters

A freelance accountant forgot to file an important tax document for a client on time. The client received penalties from the IRS and demanded the accountant cover the cost. Professional liability insurance covered the legal costs and the settlement — a situation that would have been financially devastating without coverage.

A web developer built an e-commerce site for a small business but missed specific privacy compliance requirements. When the client was later fined by regulators, they blamed the developer and filed a claim. The insurance covered the legal defense and settlement.

A marketing consultant developed a strategy for a retail client. The campaign underperformed and the client lost significant revenue. They claimed the consultant’s advice was negligent. Even though the consultant had acted in good faith with the information available, the legal process still had to run its course — and the policy covered it.

None of these professionals were reckless. All of them would have faced serious financial consequences without coverage.

The Claims-Made Structure — Why This Detail Matters

Most professional liability policies operate on a claims-made basis. This confuses people and it’s worth understanding clearly before you buy.

A claims-made policy covers claims that are filed while the policy is active — not necessarily when the work was performed.

So if you complete a consulting project in 2024 and the client files a lawsuit in 2026, your 2026 policy handles it — as long as it includes a retroactive date that covers the original work.

This has two important implications:

Maintain continuous coverage. If you cancel your policy and a claim comes in afterward for work you did while covered, you may have no protection. Gaps in coverage create gaps in protection.

Consider tail coverage if you stop practicing. Tail coverage — sometimes called an extended reporting period — allows claims to be reported after a policy ends. If you’re retiring, closing your business, or changing careers, tail coverage protects you from claims that emerge after your policy lapses.

Who Actually Needs This Coverage

Any business providing professional services or advice faces this exposure. Some industries see claims more frequently than others.

Consultants and marketing professionals — strategic recommendations directly affect client revenue. When campaigns underperform or strategies miss the mark, consultants are often first in the firing line.

Accountants and financial advisors — financial mistakes can cascade into significant losses. Even small errors in tax preparation or financial planning can generate large claims.

Technology professionals — software developers, IT consultants, and cybersecurity specialists face claims related to system failures, security vulnerabilities, and missed project requirements.

Architects, engineers, and designers — design errors can cause expensive construction problems. The scale of projects in these fields means claims can be substantial.

Freelancers and independent contractors — often the most exposed of all. Large firms have legal departments and financial reserves. Freelancers typically don’t. One significant claim can reach directly into personal savings.

If you provide a service, give advice, or deliver expertise to clients — this coverage is relevant to you.

Fiduciary Liability Insurance: Protecting Plan Managers

How Much Coverage Do You Actually Need ?

The right amount depends on the scale of your work and the financial exposure involved.

| Policy Structure | What It Means |

| $1M per claim | Maximum paid out for a single claim |

| $2M aggregate | Maximum paid out for all claims in a policy year |

For most small businesses and freelancers, $1 million per claim with $2 million aggregate is a common and reasonable starting point.

If you work with large corporate clients where project values run into the millions, higher limits make sense. A $1 million policy is meaningless protection on a $5 million project if something goes seriously wrong.

Consider the size of your largest current contract. If a total failure of that project led to a lawsuit, what would the potential damages look like? Your coverage limit should be at minimum in that neighbourhood.

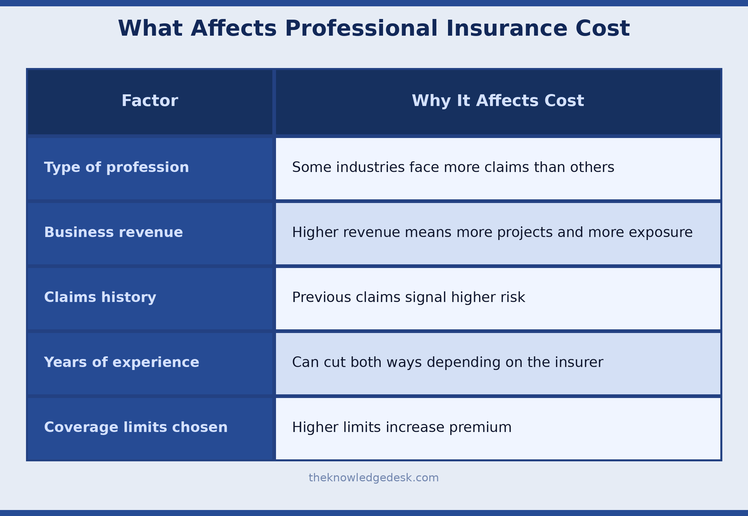

What Determines the Cost

For most freelancers and small service businesses, annual premiums run between $800 and $2,500 depending on the profession and coverage level. Businesses with employees or higher revenue typically pay more.

Put that in perspective — $2,500 per year is roughly $48 per week. One hour of legal fees in a professional liability lawsuit typically costs more than that.

What It Does NOT Cover

Intentional fraud or criminal acts — insurance covers mistakes, not deliberate wrongdoing. If you knowingly misled a client, no policy will cover the consequences.

Physical injuries or property damage — that’s what general liability is for. Professional liability is strictly about financial losses arising from professional services.

Employee disputes — harassment claims, wrongful termination, and similar employment matters fall under employment practices liability insurance, which is a separate policy.

Cyber incidents and data breaches — if client data is compromised, that’s cyber liability insurance territory. Some businesses assume their professional liability policy covers data breaches — it typically doesn’t.

Work outside your stated profession — if a policy is written for marketing consulting and you start offering legal advice, coverage for that work is likely excluded.

Employers Liability Insurance: What it is, why it matters ?

Cyber Liability Insurance: What It Covers & Why It Matters

How to Reduce Your Risk Without Just Relying on Insurance

Coverage is essential. Preventing claims in the first place is better.

Write clear, specific contracts. The scope of work, deliverables, timeline, and what success looks like should all be explicitly defined. Vague contracts create space for disagreements about what was promised.

Document everything in writing. Confirm decisions, changes, and approvals by email. A paper trail is your best defence when a client’s memory of events differs from yours.

Set realistic expectations from the start. Overpromising to win a client is one of the most reliable paths to a professional liability claim. Under-promise and over-deliver — not the other way around.

Define project start and end dates clearly. Ambiguity about when your responsibilities end creates ongoing exposure. Close projects formally in writing.

Communicate problems early. If a project is running into issues that might affect the outcome, telling the client early is almost always better than hoping it works out and explaining after the fact.

Certificate of Insurance: What They Are & Why You Need One

Frequently Asked Questions About Professional Liability Insurance

What is professional liability insurance?

It’s coverage that protects service businesses and professionals when clients claim their advice, work, or services caused financial loss — covering legal defense costs, settlements, and court judgments.

Is it the same as malpractice insurance?

Yes, conceptually. Malpractice is the term used in medicine and law. Errors and omissions or professional liability is the terminology used in most other industries. Same protection, different name.

Do freelancers really need this?

Yes — arguably more than larger businesses. Freelancers typically don’t have legal teams or financial reserves to absorb a claim. Personal assets are often directly at risk.

Does it cover false or exaggerated claims?

Yes. The policy covers your legal defense whether the claim has merit or not. Being in the right doesn’t mean the legal process is free.

Can past work be covered?

Yes, if your policy includes a retroactive date that covers the period when the work was done and the claim is filed while the policy is active.

What’s a retroactive date?

The date from which your policy covers past work. If your retroactive date is January 2022 and you completed a project in March 2022, a claim filed today against that work is covered. Work done before the retroactive date typically isn’t.

What is tail coverage?

An extended reporting period that allows claims to be filed after a policy ends — important when closing a business, retiring, or switching insurers. Without it, work done under an old policy may have no coverage for future claims.

How quickly can I get covered?

Most insurers can issue a professional liability policy within 24 to 48 hours for standard professions. Some specialised industries take longer due to underwriting requirements.

Does having a contract with my client eliminate the need for this insurance?

No. Contracts reduce risk and clarify expectations, but they don’t prevent clients from filing lawsuits. A contract is a defence — not a shield against legal action.

What’s the difference between per-claim and aggregate limits?

Per-claim is the maximum your insurer pays for a single claim. Aggregate is the maximum they pay across all claims in a policy year. If you have $1M per claim and $2M aggregate and face three claims totalling $1.5M, each individual claim is covered but your aggregate limit caps total payout.

The Bottom Line

Professional work always carries risk. Clients have expectations. Projects encounter problems. Results don’t always match predictions. And occasionally, even when you’ve done everything right, someone decides to file a claim.

Professional liability insurance doesn’t prevent any of that from happening. What it does is make sure that when it happens — and for enough service businesses, it eventually does — the financial consequences don’t end your business or follow you personally for years.

For most freelancers and small service businesses, the annual cost is less than one hour of legal fees in a lawsuit you’d be paying for out of pocket without it.

Review your contracts. Know your exposure. And make sure the coverage you carry actually matches the work you do.