Key Takeaways:

- Proof of insurance is a document confirming your policy is active — not the full policy itself

- Most US states now accept digital proof on your phone, but a physical backup is still worth carrying

- Failing to show proof during a traffic stop can result in fines of $100 to $500 — even if your insurance is active

- Different situations need different proof — drivers need ID cards, businesses need certificates of insurance (COIs), renters need declarations pages

- Some drivers with serious violations must file an SR-22 or FR-44 — a special document filed directly with the state by your insurer

- Keeping a screenshot of your insurance card in your phone’s photo gallery costs nothing and can save real headaches

Proof of insurance is a document — physical or digital — that confirms your insurance policy is currently active and valid, and without it you can face fines, delays, or legal trouble even if your actual coverage is perfectly in order.

Nobody Thinks About This Until Someone Asks For It

It usually happens at the worst possible moment.

You’ve been pulled over. Or you’re sitting at a car rental counter with a line behind you. Or a new client emails asking for your certificate of insurance before they’ll sign the contract. Or the doctor’s receptionist is waiting while you dig through your wallet.

In that moment, a small document suddenly becomes very important very fast.

Proof of insurance is one of those things people assume they’ll have when they need it — until they don’t. And the consequences of not having it ready, even when your coverage is completely current, range from inconvenient to genuinely expensive.

This guide covers everything worth knowing — what proof of insurance actually is, the different forms it takes depending on your situation, what happens without it, and the simple habits that mean you’ll never be caught scrambling for it.

What Proof of Insurance Actually Is

Think of it as a receipt for your policy rather than the policy itself.

Your full insurance policy document might run 30 to 40 pages of terms, conditions, exclusions, and definitions.

Proof of insurance is the condensed version — a small card or single-page document that gives whoever’s asking the specific information they need to confirm your coverage is real and currently active.

Most proof of insurance documents include the name of the insurance company, your policy number, the policy start and end dates, the policyholder’s name, the insurer’s contact information, and the relevant coverage details for the policy type.

That’s it. It’s not a comprehensive summary of everything your policy covers. It’s confirmation that a policy exists, who it covers, and when it’s valid.

The Different Types — Because One Size Doesn’t Fit All

Proof of insurance looks different depending on what kind of coverage you have and who’s asking for it.

Auto Insurance ID Card

This is the one most people picture. When you buy car insurance, your insurer issues an ID card — showing your name, the vehicle’s year, make, model, and VIN, the policy number, and the coverage dates.

If you’re in a minor parking lot accident and both drivers need to exchange information, the insurance card is what gets swapped. If a police officer pulls you over, it’s one of three things they’ll ask for alongside your license and registration.

Most states now legally accept a digital version displayed on your phone. Still, a printed card in the glove box is cheap insurance against a dead battery at the wrong moment.

Certificate of Insurance (COI)

Businesses deal with this one constantly. A certificate of insurance is a one-page document summarising the coverage a business carries — general liability, professional liability, workers’ compensation, commercial auto, whatever applies.

Clients and contractors ask for COIs before projects begin. A construction company won’t let a subcontractor on site without one. A corporate client won’t sign a consulting agreement without one. A venue won’t allow an event without one.

It confirms to whoever is hiring or working with you that your business is properly insured — and that if something goes wrong, there’s coverage in place to handle it.

How to Get a Certificate of Insurance

Health Insurance Card

Your health insurer provides a member ID card showing your name, plan name, group number, copay information, and customer service contact. Every medical appointment starts with the receptionist asking for it. Every pharmacy needs it to process your prescription correctly.

Keep it in your wallet. Keep a photo of it on your phone. Losing it mid-treatment creates administrative headaches you don’t need.

Homeowners or Renters Insurance Declarations Page

When a landlord requires proof of renters insurance before you move in, or a mortgage lender requires proof of homeowners coverage before closing, what they want is the declarations page — showing the policyholder, property address, coverage limits, and effective dates.

Your insurer can generate this quickly. Most have it available through their online portal within minutes.

SR-22 and FR-44

These are different from everything else on this list. An SR-22 or FR-44 isn’t something you carry with you — it’s a document your insurance company files directly with your state’s DMV, confirming you maintain the legally required coverage.

These are required after serious driving violations — DUI convictions, driving without insurance, license suspensions, and similar events. The requirement typically stays in place for several years, and if your coverage lapses during that period, your insurer notifies the state immediately and your license can be suspended again.

Why This Document Actually Matters

The reason proof of insurance exists is simple — rules only work if they can be verified.

Almost every state requires drivers to carry liability insurance. Healthcare providers need to confirm coverage before treatment. Landlords need to know tenants can cover damage they might cause. Clients need to know the contractors they hire won’t leave them exposed if something goes wrong on the job.

Without a verification mechanism, none of those requirements mean anything. Proof of insurance is that mechanism.

It also matters for practical reasons beyond compliance. When an accident happens, insurers use documentation to confirm that coverage was active at the time of the incident. Claims process faster when proof is clear and immediately available. Disputes about whether coverage existed are far less likely when the document is right there.

Common Situations Where You’ll Need to Show It

Traffic stops — the most common situation for drivers. An officer asks, you show it. Can’t show it? Fine — even if your policy is completely current.

Car accidents — both drivers exchange insurance information at the scene. Your card is how the other driver’s insurer contacts yours to process the claim.

Renting a vehicle — rental companies check your existing coverage before deciding whether to push their own insurance add-ons. Your card tells them what you already have.

Starting a new job or contract — freelancers and contractors are increasingly required to provide COIs before work begins, particularly for corporate clients or government contracts.

Moving into a rental property — many landlords now require proof of renters insurance as a lease condition.

Medical appointments — your health insurance card is standard intake information at any healthcare facility.

What Happens If You Can’t Show It

The consequences depend on the situation — but none of them are pleasant.

During a traffic stop, failing to produce proof of insurance typically results in a citation. Fines vary by state but commonly fall between $100 and $500 for a first offense. If you actually have insurance, courts will usually dismiss the fine once you show documentation — but you still have to deal with the court process to get there.

Driving without insurance at all is a different and much more serious situation. It can result in license suspension, vehicle impoundment, significant fines, and higher insurance premiums for years afterward. Some states require SR-22 filing just to get your license reinstated.

For businesses, the consequences can be more immediately financial. A contractor who can’t produce a COI may be turned away from a job site or lose the contract entirely. For a small business, that’s not just paperwork inconvenience — it’s lost income.

Digital vs Physical: What’s the Smart Move in 2026 ?

Most states now legally accept digital proof of insurance displayed on a smartphone. Your insurer’s app, a downloaded PDF, or even a screenshot in your photo gallery all count in most jurisdictions.

The advantages of digital are real — it updates automatically when your policy renews, you can email it to anyone who needs it instantly, and you can’t leave it at home.

But carrying only digital proof has risks that are easy to underestimate. Phones run out of battery. Apps fail to load when signal is poor. Some officers and officials in certain states still have a strong preference for physical documentation.

The practical answer is both. Keep your insurance card in your phone’s photo gallery where it doesn’t require an app or a signal to access. Keep a printed card in your glove box as backup. It takes five minutes to set up and eliminates the problem entirely.

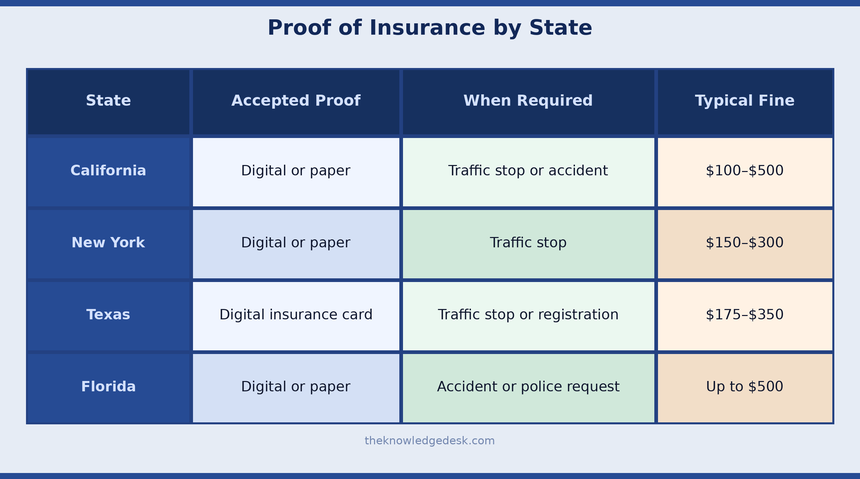

State Requirements at a Glance

Requirements vary by state, but the general pattern is consistent across the US:

Most states accept digital proof on a smartphone. If you travel between states regularly, carrying a physical card is particularly worth doing — requirements do vary at the margins.

How to Get Proof of Insurance Quickly

For auto insurance, log into your insurer’s app or website. Every major insurer — State Farm, GEICO, Progressive, Allstate, and others — lets you download or screenshot your ID card instantly. You can have it on your phone in under two minutes.

For a certificate of insurance, contact your insurance broker or agent. Most can send a COI by email within a few hours. If you need one regularly for client work, ask your insurer to set up a process for generating them quickly — many have automated systems.

For renters or homeowners insurance declarations pages, log into your insurer’s online portal. Most allow you to download the current declarations page directly.

For SR-22 filing, you don’t handle this yourself — your insurer files it with the state on your behalf. Confirm with them that the filing has been completed and ask for written confirmation that you can keep.

Simple Habits That Prevent the Problem Entirely

None of these take more than a few minutes to set up:

Keep a screenshot of your current insurance card saved in your phone’s photo gallery — not just in the app, where it might require a login or signal to access.

Store a printed copy of your auto insurance card in your glove box. Replace it when your policy renews and a new card arrives.

If you run a business, keep a folder — physical or digital — with current COIs for every active client relationship. Know when each one expires.

When your policy renews, check that the new card shows the correct dates and information before discarding the old one.

If you ever switch insurers, confirm your new policy is active before cancelling the old one. Even a single day of lapsed coverage can cause problems — particularly if you have an SR-22 requirement.

Frequently Asked Questions About Proof of Insurance

Is digital proof of insurance legal? In most US states, yes — you can show your insurance card on your phone during a traffic stop. A handful of states have specific rules, so carrying a physical backup remains sensible, especially when travelling.

What if my card shows an expired date? Your policy may have renewed but the new card hasn’t arrived yet. Contact your insurer immediately and request updated documentation. Don’t assume the officer or official will take your word for it.

Can someone else use my insurance card? No. Insurance cards are tied to specific vehicles and specific policies. Using one for an unrelated vehicle is insurance fraud, which carries serious consequences.

How long should I keep old insurance documents? A minimum of three years is a reasonable guideline. Old documentation can be important if questions arise about past claims, coverage gaps, or disputes about whether coverage existed at a specific date.

What exactly should I send a landlord asking for proof of renters insurance? The declarations page from your renters insurance policy showing your name, property address, coverage limits, and effective dates. Your insurer can generate this quickly from their online portal or by calling them directly.

What’s the difference between a COI and an insurance card? An insurance card is for personal coverage — primarily auto insurance. A certificate of insurance is a business document that summarises commercial coverage for clients, contractors, or project partners who need confirmation that a business is insured.

What happens if I’m in an accident and can’t show insurance? Even if your policy is active, not having documentation creates immediate complications. The other party may involve police. You may receive a citation. Getting your insurer on the phone quickly to confirm active coverage is your best immediate move.

Does proof of insurance expire? Yes — it reflects the dates of your current policy period. When your policy renews, you get new documentation with updated dates. Old documentation from an expired policy period isn’t valid proof of current coverage.

The Bottom Line

Proof of insurance is one of those things that feels like a minor administrative detail right up until the moment it isn’t.

A traffic stop with no proof costs you a fine and a court date even if you’re fully covered. A client who can’t get your COI doesn’t sign the contract. A landlord who doesn’t receive your declarations page doesn’t hand over the keys.

The fix is genuinely simple — keep a screenshot on your phone, a card in your glove box, and know where to find whatever your specific situation requires. Five minutes of setup now prevents real problems later.

Your coverage is only as useful as your ability to prove it exists when someone asks.