Nobody starts a business thinking about insurance. You’re thinking about your product, your clients, maybe your cash flow. Insurance feels like one of those boring boxes you tick and never look at again.

But here’s the thing. As soon as you hire your first employee (even part time, even temporarily), you are legally responsible for what happens to them at work. You could be facing fines or lawsuits or bills that could actually destroy the business if something goes wrong and you’re not insured.

That’s what employers liability insurance is for. Not glamorous, not exciting, but absolutely worth understanding properly. So let’s walk through it.

What Is It, Really ?

Employers liability insurance protects your business if an employee claims they were injured or became ill because of their work — and they hold you responsible.

Think about a warehouse worker who throws out their back lifting boxes day after day. They might argue the company never gave them proper training or the right equipment. If they take that claim to court, you’re looking at legal fees, expert witnesses, and potentially a large compensation payout. Employers liability insurance covers all of that.

It’s worth being clear on what makes this different from other types of business insurance. Public liability covers claims from customers or members of the public. Employers liability is specifically for your staff. If your employee trips over a loose cable at work and blames you — that’s what this policy is designed for.

Is It Actually the Law?

In the UK, yes.

Under the Employers’ Liability (Compulsory Insurance) Act 1969, most businesses with employees must have this insurance in place. The minimum coverage required is £5 million, though most insurers offer £10 million as their standard — because serious claims can get very expensive, very fast.

The Health and Safety Executive enforces this. If you’re caught operating without valid coverage, you can be fined up to £2,500 for every single day you’re uninsured. There’s also a separate fine of up to £1,000 for not displaying your certificate of insurance where staff can see it.

In the United States it works differently — employers liability coverage is usually bundled inside workers’ compensation policies, and the rules vary by state. But the principle is the same: if someone gets hurt at work, there needs to be a system in place to deal with it.

Who Doesn’t Need It?

There are a few exceptions, though they’re narrower than most people assume.

- Sole traders working completely alone — no employees at all — generally don’t need it.

- Some family businesses where every employee is a close relative and the business isn’t a limited company may qualify for exemption.

- Public sector organisations and certain government bodies are exempt because government funding covers any compensation.

But the moment you bring in even one part-time worker who isn’t a close family member, you almost certainly need coverage. If you’re unsure, assume you do — the consequences of getting it wrong are too costly.

What Does It Actually Cover?

Two main things: compensation payments and legal costs.

If an employee wins a claim against you, the policy pays the compensation — which can include their medical expenses, lost earnings, and damages for pain or suffering. But even if the claim fails, you still need solicitors, and that alone can cost tens of thousands of pounds. The policy covers that too.

The kinds of claims that come up most often include:

- Physical injuries — slips, falls, equipment accidents, lifting injuries.

- Occupational illnesses — hearing damage from machinery, breathing problems from hazardous materials, repetitive strain injuries.

- Mental health claims — stress-related illness caused by excessive workload or unaddressed bullying. These are becoming much more common.

One thing that catches a lot of businesses off guard: claims can surface years or even decades later. An employee exposed to asbestos or harmful chemicals might not develop symptoms until long after they’ve left. That’s why employers are required to keep their insurance certificates for up to 40 years.

What It Doesn’t Cover

Just as important as knowing what’s included is knowing what isn’t.

- Injuries to customers or visitors — that falls under public liability insurance.

- Employment disputes like unfair dismissal, discrimination, or harassment — that’s employment practices liability, a separate policy.

- Intentional harm caused by management or the employer.

- Road accidents while staff are driving for work — motor insurance handles that.

Gaps in coverage are how businesses get into serious trouble. It’s worth reviewing all your policies together to make sure nothing falls through the cracks.

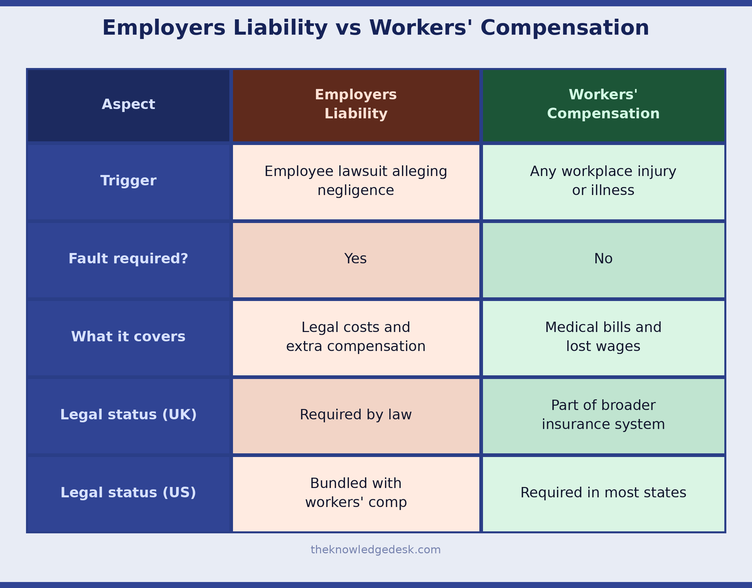

Employers Liability vs Workers’ Compensation — What’s the Difference?

People mix these up all the time, so here’s the clearest way to think about it.

Workers’ compensation pays out when an employee is injured at work, regardless of blame. It’s quick, it’s relatively straightforward, and it covers medical costs and lost wages.

Employers liability kicks in when the employee goes a step further and claims you were negligent — that you caused or contributed to their injury through poor training, unsafe conditions, or bad equipment. That’s when it becomes a lawsuit, and that’s when the costs can get serious.

Together, the two create a full safety net. Separately, each one leaves gaps.

Commercial Condo Insurance: What Owners Often Miss

Renters Insurance 2026: Essential Protection for US Tenants

What Does It Cost?

There’s no single answer because premiums depend on a few key things.

- The type of work your employees do. Office staff are low risk. Construction workers, manufacturers, and farm workers are much higher risk — and premiums reflect that.

- Your total payroll. Insurers use this as a rough measure of how much workforce exposure you have.

- Your claims history. A string of past accidents will push your premiums up. A clean safety record brings them down.

For a small office-based business in the UK, annual premiums might sit somewhere between £150 and £500. For a mid-sized construction firm, it could be several thousand pounds.

The good news is that investing in proper safety training, regular risk assessments, and decent equipment doesn’t just protect your people — it also signals to insurers that you’re a lower risk, and your premiums reflect that over time.

A Few Real Claims That Show Why This Matters

It’s easy to think of workplace injury claims as edge cases. They’re not.

A warehouse worker in Manchester suffered serious back injuries because of repeated heavy lifting without adequate training or equipment. The total claim — medical costs, lost earnings, damages — came to over £200,000.

An office worker developed chronic wrist pain after years of working at a poorly set up desk. The employer settled the claim once it became clear the workstation didn’t meet basic ergonomic standards.

A manager successfully claimed stress-related illness after sustained pressure and a complete absence of management support. Mental health claims are now one of the fastest-growing areas of employers liability litigation.

None of these are unusual. None of them happened in dangerous or unusual workplaces. They happened in warehouses, offices, and meeting rooms exactly like yours.

What Does Liability Insurance Cover ? A Complete Breakdown

How to Stay on the Right Side of the Law

A few practical things to keep in mind.

- Make sure your policy is active and provides at least the minimum required coverage — £5 million in the UK, though £10 million is far more sensible.

- Display or make available your certificate of insurance so employees can actually see it. This is a legal requirement.

- Keep your old certificates. Occupational illnesses can appear decades later, and you need to be able to prove you were covered at the time.

- Run regular safety training and workplace risk assessments. Not just for legal reasons — because it actually reduces claims, and lower claims mean lower premiums.

The Gig Economy Complication

If your business uses freelancers, contractors, or gig workers instead of traditional employees, don’t assume you’re off the hook.

Courts have increasingly found that workers who operate under a company’s control — even without a formal employment contract — may be classified as employees for legal purposes. The Uber BV v Aslam ruling in the UK is the most well-known example, where drivers were recognised as workers despite being officially classed as self-employed contractors.

If your freelancers work regular hours, follow your processes, and use your tools, a court might see them as employees too. It’s worth getting proper advice on how your workforce is classified before you assume you’re exempt.

The Bigger Picture

Look, most people buy employers liability insurance because the law says they have to. That’s fine. But there are real benefits beyond just staying compliant.

Employees notice when a company takes their safety seriously. It builds genuine trust, reduces turnover, and makes recruiting easier. Clients and investors also tend to view properly insured businesses as more professional and more stable.

And then there’s the simple financial reality. One serious injury claim, without insurance, could wipe out a small business entirely. The premium you pay each year is a fraction of what a single bad claim could cost you.

In most countries, including the UK and US, those premiums are also tax-deductible as a legitimate business expense. So there’s really no argument for skipping it.

Quick Answers to Common Questions

Do small businesses need it?

Yes. Even one part-time employee triggers the legal requirement in the UK.

Does it cover remote workers?

Yes. Your responsibility for employee safety doesn’t disappear when they work from home. If they injure themselves using work equipment or because of a workstation problem linked to their job, you may still be liable.

Is £5 million enough?

It’s the legal minimum, but most insurers recommend £10 million as standard. Serious claims can exceed the lower figure.

Does it cover mental health claims?

Yes, if your negligence contributed to the condition. This area is growing fast.

Are premiums tax deductible?

Yes — in the UK and US, they count as a business expense.

The Bottom Line

Employers liability insurance isn’t the most exciting part of running a business. But it’s one of the most important.

It protects you from the kind of legal and financial exposure that can genuinely destroy a company. It protects your employees by ensuring there’s a proper system in place if something goes wrong. And it keeps you on the right side of the law.

Get the right level of coverage. Keep your certificates. Invest in proper safety practices. And then get back to actually running your business — knowing that if the worst happens, you’re covered.